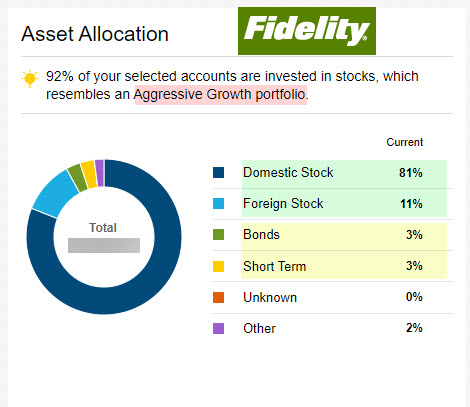

Aggressive Growth Portfolio

An “aggressive growth portfolio” doesn’t have to be a stupid, risky, portfolio. However, being aggressive means: 1) You have to have a willingness to ride a roller coaster market, 2) Have a sharp understanding of your reasons for buying and holding an investment, and 3) Emotional fortitude to weather sharp declines in the overall stock market. It isn’t for the faint-hearted. This image shows our current investment allocations. Note that 92% of our assets are in stocks (and stock ETFs), and that bonds and cash are currently around 6%. That will change in the next couple of weeks as I buy additional stocks and stock ETFs.

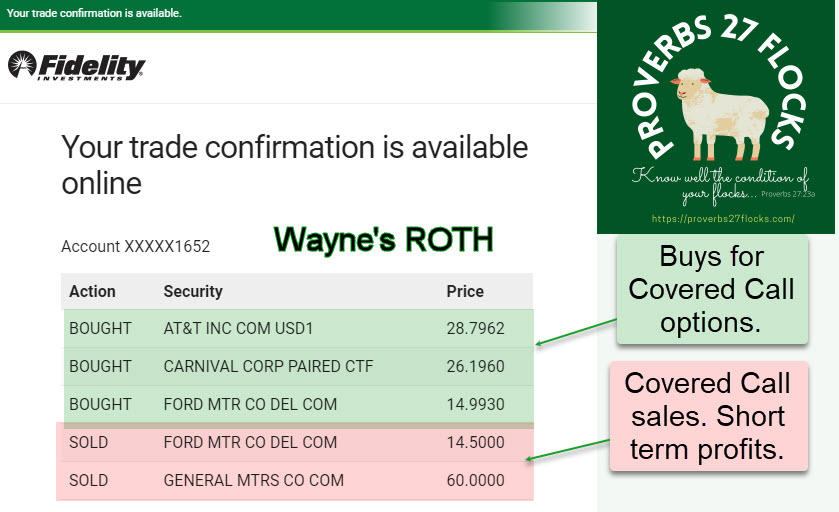

Covered Calls Called Away

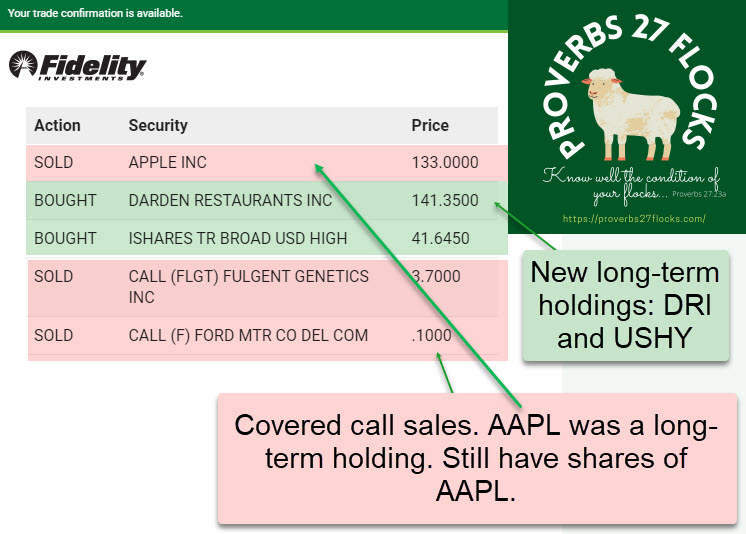

I gave up my long-term holding of 100 AAPL shares at a fair price and a tremendous profit. We still own AAPL, so I am not done with that investment. Other short-term positions were also called away. I buy short-term positions of Ford (F) and General Motors (GM). I then sell covered calls for a price greater than my purchase price. That gives me income from the covered call plus the short-term income from the sell price profit.

New Investments: A Restaurant and a Bond ETF

I purchased 100 shares of DRI (Darden Restaurants, Inc.) using a buy limit order. This will be a long-term dividend growth investment in our portfolio. With the post-Covid recovery well underway, I see potential for good growth in this investment as well.

I also purchased 100 shares of USHY (iShares Trust – iShares Broad USD High Yield Corporate Bond ETF) for my traditional IRA. Bonds are a part of our portfolio of investments, but a very small part. I like USHY because it offers monthly income with a decent yield of 5.19%. The expense ratio is a sane 0.15%. The ETF grades on Seeking Alpha are solid for momentum, expenses, dividends, risk, and asset flows.

Other Short-term Buys

You will also notice some short-term buys. I buy investments like CCL (Carnival Corporation & plc) so that I can use the shares for covered calls. I do repeat buys of Ford and AT&T for the same reasons.