Why Inflation Will Surprise Many

Investors who know the scriptures know that the book of Revelation talks about dramatic future final events. I don’t subscribe to the various writers who have “predictions” that try to forecast the future based on a single statement in the Bible. I have heard all kinds of crazy predictions about the end of the world using the “Bible” as proof. So far, all of them have been wrong. Many of them try to define the “when” of events and even err in their interpretation of the “what.” There is, however, a surprising statement about the future in Revelation 6:6: “A quart of wheat for a denarius, and three quarts of barley for a denarius, and do not harm the oil and wine!”

In the time of Jesus, the disciples would have been able to purchase a loaf of bread for 0.04 denarius. A denarius is a day’s wages for the typical worker. Therefore, a common laborer could potentially buy 25 loaves of bread for a day’s wages. That is why the prophecy in Revelation would have shocked the first century reader. This talked about run-away inflation in the price of a loaf of bread. (Mark 6:35-6:44 makes it clear that the disciples thought it would take 200 days of wages to buy 5,000 loaves of bread.)

We need to translate this into terms we understand. I think I could buy one loaf of bread today for $2.00. A good bread would be more like $5.00. Inflation like the one expressed in Revelation 6:6 would mean that I would have to pay $50 for a $2 loaf of bread or $125 for a $5 loaf. Even supposing that you don’t believe the scriptures, remember that I used to go to the grocery store for my mom and could buy a loaf of bread for $0.19 in the early 1960’s. Today I have to pay more than ten times that amount.

Here is Why This Matters

The sad reality is that you cannot afford to “play it safe” and keep your retirement investments in cash and bonds. That is a losing battle. Using a broad index mutual fund or ETF is far more prudent. However, there are some risks in this approach as well.

Using Index Funds

As I mentioned in some previous posts, using an index fund that tracks the S&P 500 or the NASDAQ have risks that might not be obvious. For example, the top ten holdings in funds like this tend to be some heavy hitters in technology that can fall out of favor. This has happened recently with several big technology names. This increases the downside risk for ETFs like SPY, VOO, and IVV. Each of these tracks the S&P 500. Each of them has about 500 companies that are great investments (most of the time.)

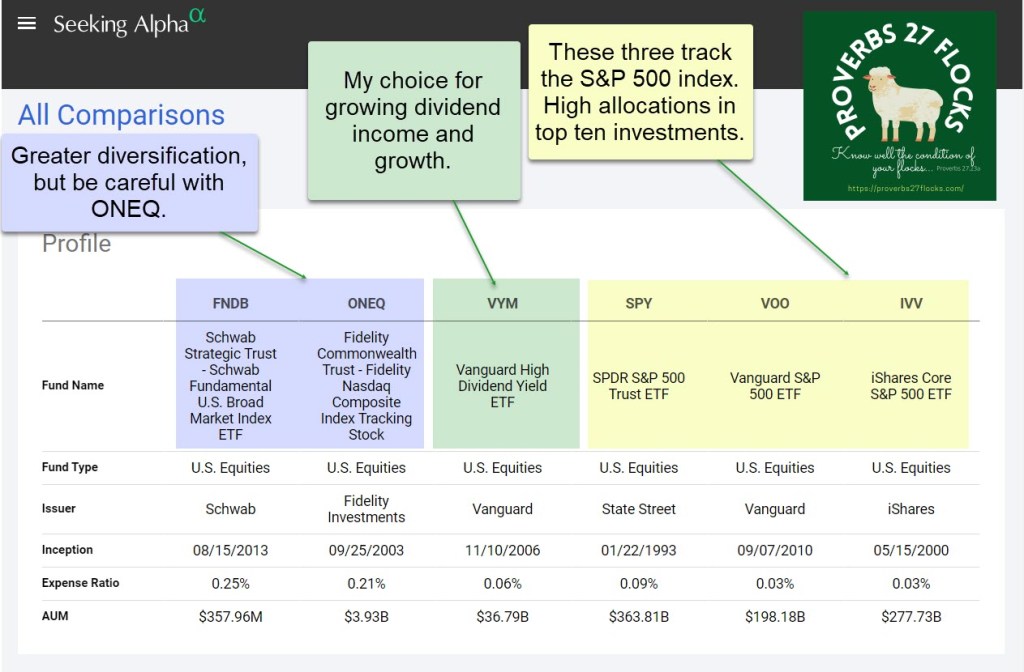

Compare FNDB ONEQ VYM SPY VOO IVV

If you want to decrease your risk, you may want to expand beyond the S&P 500. Three ETFs to consider include FNDB, ONEQ, and VYM.

FNDB is the Schwab Strategic Trust – Schwab Fundamental U.S. Broad Market Index ETF. This has some appeal because it has 1,673 holdings. The expense ratio is higher than SPY, VOO, IVV, but it isn’t terrible. The five-year returns are “less” than those of the S&P 500 index, so I’m not suggesting that you abandon the S&P 500 funds. Rather, think about changing your allocation to that narrow range of investments.

ONEQ is the Fidelity Commonwealth Trust – Fidelity Nasdaq Composite Index Tracking Stock. This fund has an amazing ten-year history of 368%, far better than “SPY VOO IVV.” There are 1,021 investments in this fund and the expense ratio is acceptable.

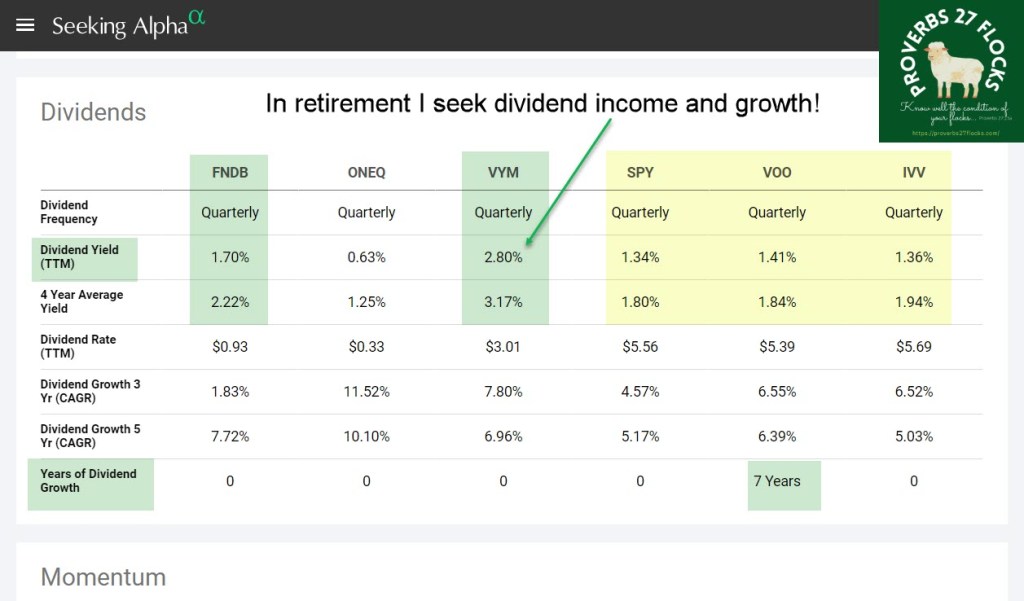

VYM, as my readers know, is a fund I use in our retirement accounts because I want income and investment growth. VYM is the Vanguard High Dividend Yield ETF. The yield is solid and there are 417 stocks in this ETF.

One Final Thought: Simple Moving Average (SMA)

Due to the beating the top technology stocks have taken recently, ONEQ, SPY, VOO, and IVV have a lower 200-Day SMA than FNDB and VYM. The 200-Day SMA covers roughly 40 weeks of trading. It is commonly used in stock trading to determine the general market trend. As long as a stock price remains above the 200-day SMA on the daily time frame, the stock is generally considered to be in an overall uptrend. Look at the following images to see some of the data I have highlighted.

Conclusions

First, don’t be blind-sided by inflation. If you don’t invest in stocks, inflation will be your enemy. Bread will be expensive when you retire. Count on difficulties twenty years from now if you stick with a “conservative, safe, investment mix.” Secondly, give some thought to the reasons you buy and hold the mutual funds and ETFs in your retirement accounts. Mistakes can be costly. Finally, read the book of Revelation after you read the Gospel of John. Both were written by the same author. John knew Jesus and he knew Jesus was his only long-term hope and future.

LINKS for related discussions:

The Top Heavy NASDAQ

A Common Mistake is Large Cap Investing