Do You Measure It?

If you have ever worked with a financial advisor or signed up online for a brokerage or retirement account, one of the questions you will be asked is “what is your risk tolerance?” It is something akin to being asked, “how much short-term pain can you endure before you scream and run?” Most of the time the difference between volatility and investment risk are not clearly defined. As a result, far too many fall into the trap of wanting to be “conservative” in their investing approach. This is a short-term strategy that ignores long-term realities.

Sources or types of Risk

Some of the more common risks are business and industry risk, inflation risk, market risk, liquidity risk, interest rate risk. These can be driven by bad management calls or an industrywide slowdown. Inflation can gnaw away at your spending power over time. Perhaps the general market or economic environment will cause the investment to lose value regardless of the particular investment. Your investment may drop in value simply because the overall stock market has fallen. Liquidity risk is a danger homeowners face. If you need to sell your home in an emergency, and no one is buying, you face this risk because there are no buyers.

Measuring Your Appetite for Risk Using a Tool

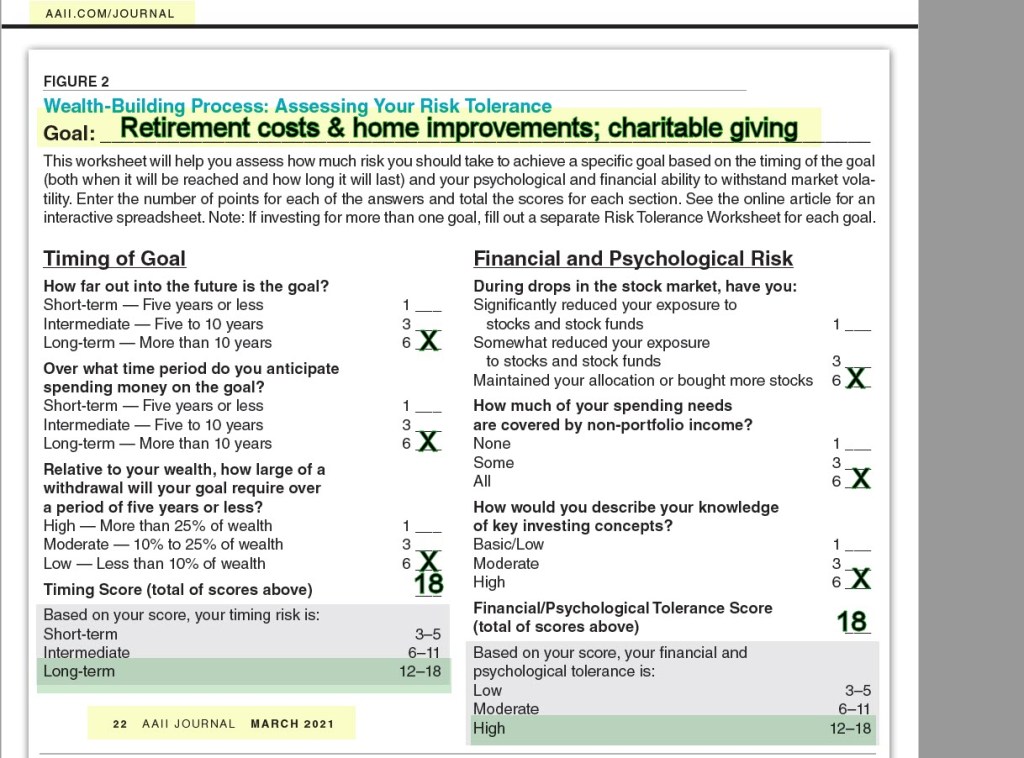

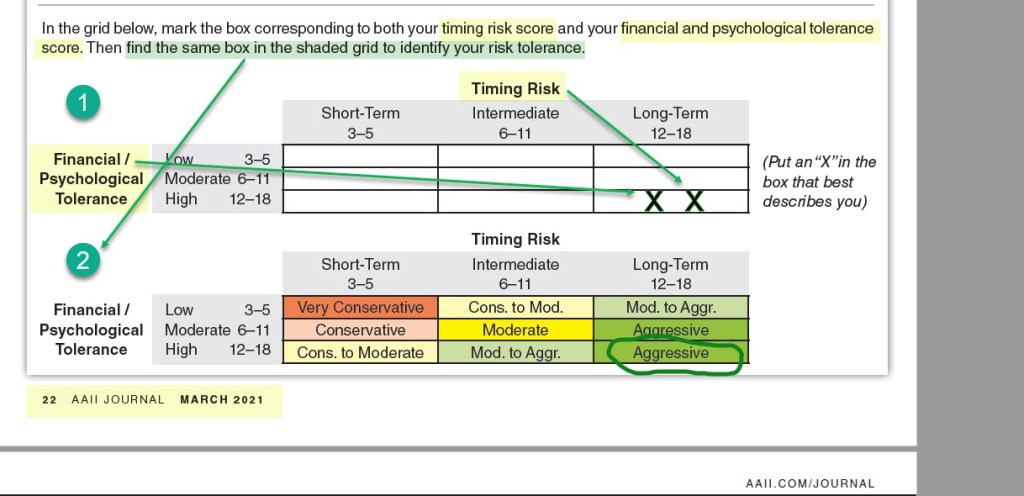

There are at least two key factors to consider. One is called timing risk. That is the risk that you need to take money from your investment portfolio at an inopportune time. The second is your emotional reaction to market and investment turmoil. This is your financial/psychological tolerance.

AAII has a nice tool that helps an investor determine where they fall based on specific goals. In the March 2021 AAII Journal a worksheet was provided. I completed the worksheet to illustrate how I respond to risk, which then helps me define the types of investments I will purchase for our retirement accounts.

One question you might be able to answer best by considering your past reactions and behaviors. During past market drops, did you reduce, maintain or increase your exposure to stocks? This is a better indicator than asking you how you feel today. Perhaps you are chagrined by past reactions and vow to not repeat them. Perhaps you have learned your lesson. Many risk questionnaires ask “how comfortable you would be if your portfolio fell by 25% in value?” You might feel this is too much or you might think, “I can handle that!” The real proof is in how you have behaved in the past. (Education can change your views!)

Formulating a Plan

Every investor should establish a strategic plan to guide the tactics used to implement your strategy. AAII provides “A Lifetime Strategy for Investing” as a guide for AAII members can read online or download that provides an overview for formulating a strategy given your stage in life

www.aaii.com/lifetimeinvestmentstrategy

The statement of your goal needs to be something more concrete than, “I want to be successful.” That is not measurable, nor does it incorporate any time element. Rather, you might want to start with at least a basic statement like, “I want my accounts to grow by 8-10% per year in the next ten years.” This plan will have a different view of risk and a better reaction to market volatility.