First Some History to Set the Stage

Many things have changed since I placed my first trade to buy a company’s stock. My first brokerage account was with Robert W. Baird & Co. Incorporated in Milwaukee, Wisconsin. The account was opened March 18, 1998. Universal Foods Corporation was my employer, and my manager gave me stock options as a management incentive. The 3,000 shares were for Universal Foods Corporation stock, where I worked as the Director of IT Operations. I sold some of the options in March 1998 and bought shares in three companies: Compaq Computer, Southern Co., and Pfizer. This was a very laborious process. The “broker” had to do the trades for me, and “online access” cost $25 per year without the ability to trade. Furthermore, I had to pay the broker a commission for every trade. The commission for CPQ, SO, and PFE was $286.70. Let that sink in. Back in those days I was paying a commission of about 3%. In addition, Baird charged me $4 per trade, or $12, for “postage.”

Baird’s Bad Recommendations

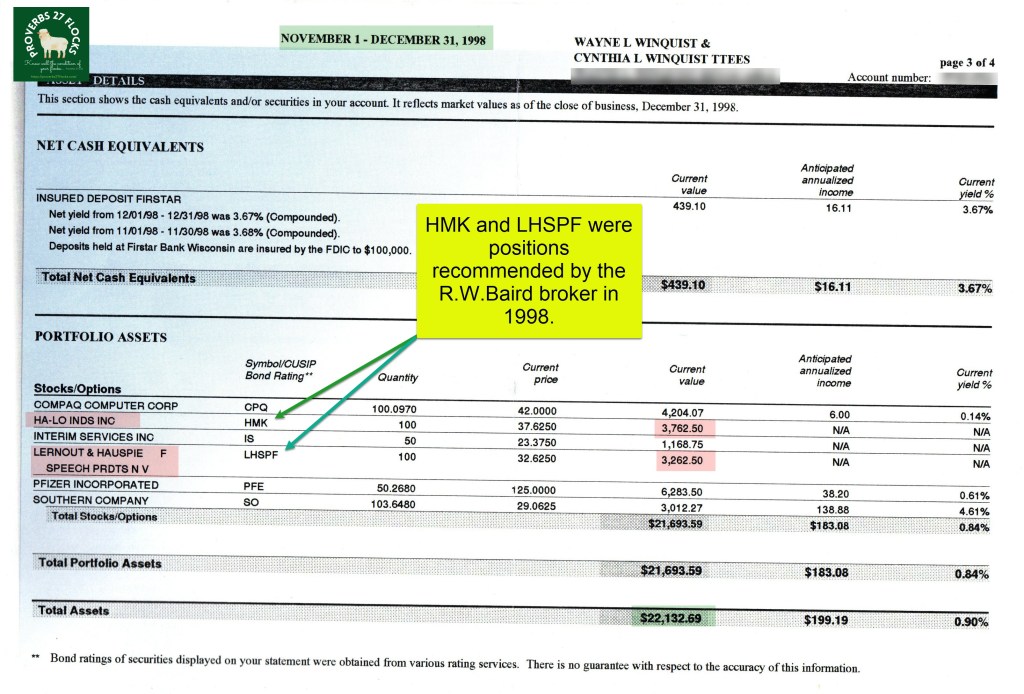

To make matters worse, the Baird broker started recommending investments in companies that were financial disasters. He offered me a “commission free” trade to entice me to buy shares of HA-LO Industries, Inc. He also sold me on the idea of Lernout & Hauspie Speech with some awful commission charges. My total cost for all of those shares was $7,543.50. To put this in perspective, these two companies represented 36% of my total investment dollars in 1998. Both companies went bankrupt for different reasons and I lost the entire investment. When you consider that I invested in six companies, having one third of them go bankrupt is incredible. In hindsight, I see how foolish I was and how poor the advice I received was. In April 1999 I resigned my position at UFC and took a job at Conney Safety Products in Madison WI. In September 1999 I opened my rollover IRA account at Fidelity Investments.

Eventually I opened my brokerage account at Fidelity too, and moved the Baird investments to Fidelity. The world was broken then, the market was broken then, and I was not an educated investor. Little has changed in the world, but the stock market has changed dramatically. In many respects it is better and faster. In other respects, it is quite broken.

What is a Broken Market?

I view a broken market as a market that is behaving like today is the only day that matters. This type of market is driven by the latest Twitter feed, today’s presidential executive order or a spike in the number of Covid-19 deaths. It is also a market that has a worldview that says “eat, drink, and be merry, for tomorrow we die.” In other words, many investors don’t have a long-term view. As the number of these retail investors increases, and as trading becomes more automated, the potential for disaster driven by short-term emotions and thinking increases.

In 2012, Sal Arnuk and Joseph Saluzzi, co-founders of equity trading firm Themis Trading LLC wrote a book about “broken markets.” (Broken Markets: How High Frequency Trading and Predatory Practices on Wall Street Are Destroying Investor Confidence and Your Portfolio.) I have not read the book, but the book’s title provides the obvious clue: the speed and ease of trading can create strange, wild, and volatile market behaviors. This makes investors nervous. Furthermore, far too many investors are driven by fear, greed, and operate in sad ignorance of some basic rules of wise investing. Some borrow money to invest and many have a get-rich-quick mentality. The emotions and irrational thinking drive behaviors that are laden with appalling risks.

So, what are the problems and what is an investor to do?

The Problems: Short-term Fixes by Short-sighted Leaders

A friend recently sent me a link to an article by Andrew Stuttaford dated January 22, 2021. This article highlights the concerns about government and central bank tampering with the market by fixing it with various types of stimulus. The lower interest rates create a hunt for yield, especially for those who are retired and desire income from their investments. Furthermore, the specter of rising income taxes, profligate government spending, and rapid inflation seems likely. All of these make every dollar earned worth less. No one wants to live within their means, and everyone wants the government stimulus checks. “Let someone else, like the wealthy, for example, pay for it!”

How then shall we live?

After reading the article mentioned above, regarding the broken market and “rational” bubbles, I wrote back to my concerned friend, who is also a believer in a Sovereign God. The Sovereign God is not ignorant of the current situation. I told my friend that my thoughts about how I invest have not changed. Rather, the article continues to cause me to want to continue to stay invested and to recognize in doing so that there will be some nasty surprises with some significant dips in the prices of stocks, bonds, and anything else that is traded. That is due to the greed/fear cycle that often feeds on itself time-after-time. We need to face certain realities about Federal monetary policy, income taxes and inflation.

We cannot fix Federal monetary policy so don’t let that control you. The Fed provides short-term fixes but creates potentially terrible consequences in taxation and inflation. The article’s author wisely notes that low interest rates drive people to the market to get a better yield, especially in retirement. Believers should avoid a short-term perspective when it comes to life and relationships. However, when it comes to material resource, our perspectives should be both short-term and long-term. It should be short-term recognizing the brevity of our lives, but it should be long-term when viewing things for eternal investments.

What can you do about taxation and inflation? Not much. There will be, in my opinion, greatly increased inflation as a result of easy money that creates more federal debt that requires higher taxation. That causes me to want to stay in the market. When I am out of the market, I cannot keep pace with inflation. I will also need more dollars to live if taxation increases, as I believe it will have to increase and President Biden’s administration will want to increase taxes on the “rich.”

Supply and Demand has an impact on the market. The number of retail investors is increasing. The platforms for trading cheaply have dramatically increased and the relative ease of and low barriers to trading electronically increased the pool of investors. In addition, international investors seem to be doing more to engage in the US stock markets and they don’t need a US-based brokerage account to do so. For example, I recently provided one-on-one investment training for a Christian lady in New Zealand who read my blog and started asking questions. Apparently New Zealand has now made it easier for retail investors to buy and sell investments in the USA. The law of supply and demand can easily drive up the price of investments and cause the P/E ratios to seem irrational based on past metrics.

Maintain both a long-term and eternity view of your investments. I will keep my eternity glasses on. While I am concerned that our government and our people have chosen a trajectory not unlike the one that has been repeated by the Israelites in the book of Judges, the Romans as their era of influence imploded, and the clear downward spiral of the European nations who have embraced a worldview that excludes God in all matters, (including those related to stewardship of what we only have by God’s grace) I make a conscious decision to trust God and not worry.

I am not fearful. I am not worried. In Christ I am secure forever. We have no need to be greedy. We need to set our minds against that natural sinful tendency. To keep a balanced view, Cindie and I have fought against that monster by increasing the giving we have been doing to individuals and ministries. For those who are fearful, I would say that cash is a losing strategy. To those that are greedy I would say that their idol will not satisfy but will disappoint.

End Note

If you don’t have the same sense of peace, assurance, and contentment, then perhaps you are trusting a god that is sightless, legless, armless, and unaware of your needs. Let me encourage you to read the Bible. Start with the Gospel of John or the Apostle Paul’s letter to the Romans. You won’t regret hearing about some good news that can transform your life, your thinking, your purpose for living, and your eternity.

Article Link: A BROKEN MARKET