Social Security is an Annuity

One of my least favorite “investments” is the annuity. I spent quite a bit of time learning about annuities when I learned that my mom had annuities in her investment portfolio. Her annuities weren’t bad, and they brought her piece of mind, but I would hardly call them an investment. It is best to think of them as insurance. In a similar way, Social Security is a guaranteed lifetime income stream backed by the full faith and credit of the U.S. Government. It’s a government issued annuity. You pay premiums during your working years with dollars that never enter your bank account. When you retire, you start to draw on your Social Security annuity.

The Fine Print

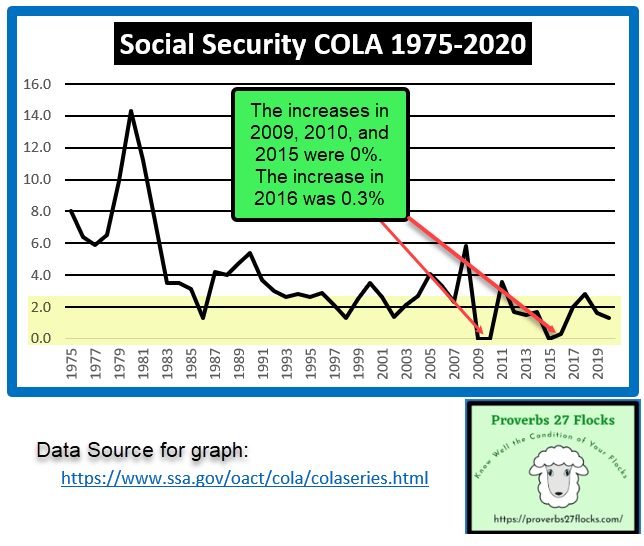

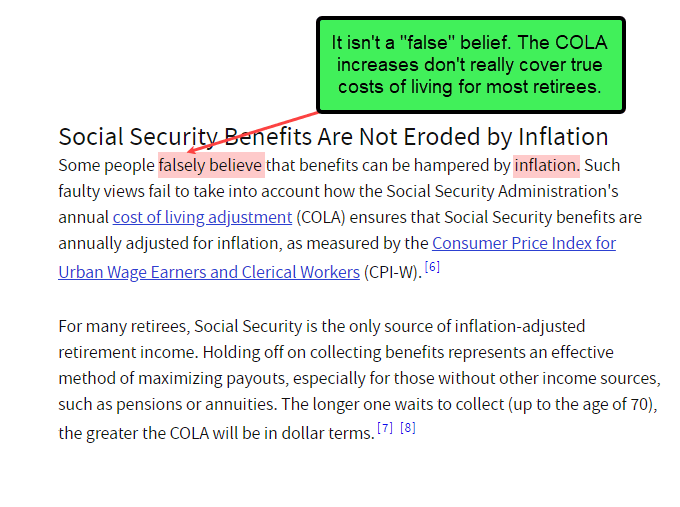

As much as some would like to have you believe, Social Security does not keep up with the typical costs of living. In recent years, the adjustment for inflation and the cost of living has been zero or practically zero. Therefore, like most annuities, it has no hope of growing like most investments that I typically purchase. This is not a complaint, but it is a statement of reality.

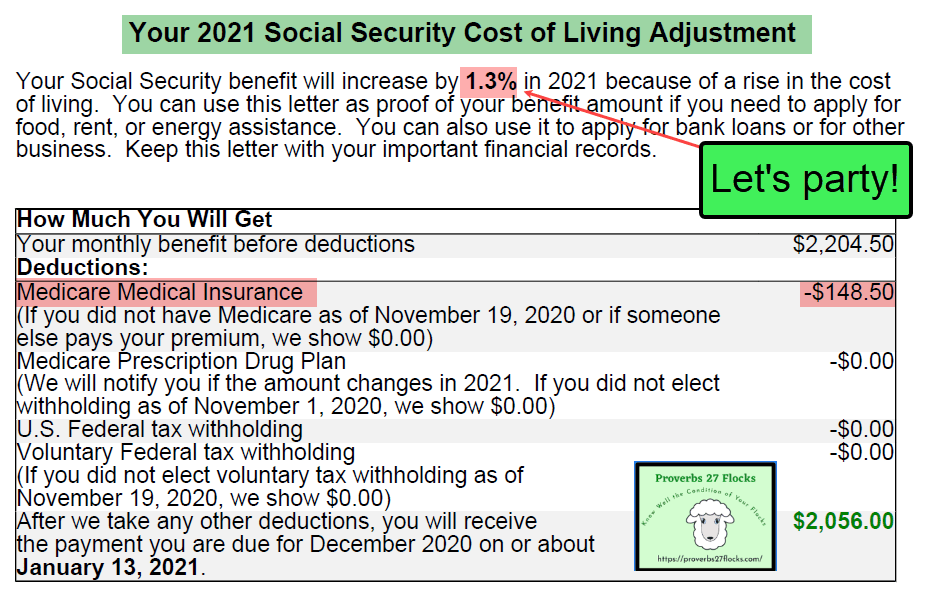

Furthermore, be aware that the government’s Medicare Medical Insurance is not free. In my case it is about $150 per month, and that is automatically deducted from my Social Security. That works out to $1,800 per year. The value I receive for that payment is good, but understand that you don’t get to keep your entire social security monthly payment. Furthermore, if you have income other than Social Security, including required minimum distributions from a taxable IRA or 401(k) account, you will likely pay income taxes on your Social Security as well. LINK: Social Security Increases. https://www.ssa.gov/oact/cola/colaseries.html

Our 2021 Social Security Increase

Drum roll please. The increase for next year is an amazing 1.3%. That means, after the Medicare insurance deduction, our increase will be $25 per month. Let that sink in. Then remember that Cindie and I will probably have a total income increase of well over 10% next year due to investment income from dividend growth alone. The government can’t and won’t be able to match our investment income growth in any year. Therefore, while I like the monthly income from Social Security, it is nothing more than a rather lackluster annuity.

What Should You do Before You Retire

Let me encourage you to think of Social Security as something you might receive if you live long enough. We can assume you might make it to age 75-80. Therefore, if you can live at what most would consider to be near the poverty level in the United States for ten to fifteen years, you can do nothing. In our case, my Social Security does cover our housing costs which are about $1,000 per month (property taxes, trash pickup, utilities, property insurance), groceries, auto insurance, fuel for our Ford Escape and a small amount of charitable giving.

In most places in this world, that would be a standard of living most do not enjoy. But while it is almost sufficient, it would be impossible to do the things we want to do if God permits. Those things would include travel, blessing family members with gifts, assisting others less fortunate than us, dining at restaurants, hobby supplies, cell phones and computer services. We can be content with less, but because we were prudent during our working years, we currently have many more choices.

My Suggested Three To Do’s

Watch the ants to see what they do. If you haven’t already done so, you should take care of the following before you retire. Don’t wait until you are 55 or 60 or 65 to do these things. Do them now.

1) First, sign on to your Social Security account and find out what your “full retirement” benefit will be. Then look at your budget. Is everything covered? Probably not. Oh, you do have a budget, right?

2) Next, look at all of your debt and develop a plan to get rid of it before you retire. Car payments, credit card payments and mortgage payments are nothing but trouble for someone in retirement.

3) Finally, look at the way you spend, save, and invest your current income. If you don’t have a plan, then be prepared for some tough days ahead. If you like danger, you will be happy.