Buying An Investment Outside of My Rules

I rarely buy an investment with attributes that fall outside of my buy list requirements. Not too long ago, a friend suggested two investment possibilities: CARR (Carrier Global Corporation) and RKT (Rocket Companies, Inc.). I like investing in disruptive business models if it looks like the company’s potential to gain market share and leverage the internet to provide a level of service for a large population of potential clients. After reviewing both CARR and RKT, I started to watch the news and prices.

What I like about CARR and RKT

While neither of these companies is very appealing from a dividend or dividend-growth perspective, both likely have long-term prospects of share price appreciation. CARR, as an industrial, has certain seen good price appreciation. CARR’s P/E is reasonable and both Seeking Alpha and Wall Street analysts are generally bullish on the stock. I am less likely to buy CARR simply because their dividend prospects are poor, and I have some better industrials in our portfolio.

Rocket, on the other hand, is a new kid on the block. As one Seeking Alpha author says (quote below), RKT has a disruptive digital footprint for a solution that usually requires a lot of work and paperwork. It can be fun to buy a home, but it is also a huge pain to deal with a bank or a traditional mortgage provider. Cindie and I have had multiple home mortgages over the years, and none of them was fun. Thankfully, we saw a need to pay off our mortgages ahead of schedule, so we escaped the monthly house payments and the tyranny of companies that sold our mortgages to other companies. While RKT doesn’t (yet) pay a dividend, I believe it has a significant opportunity to grab market share, especially from the digital-savvy younger home buyers.

Seeking Alpha Author’s Opinion

“Overall, I am bullish on the company as I believe that the historical mortgage industry is slow, heavily manual, and frankly frustrating for customers. Rocket has been able to disrupt this via a full-stack digital platform that covers everything from lead generation to underwriting, to automated processing. This processing automation is key to the company’s success. As an example, this technology enables higher loan throughput per team member as well as higher customer satisfaction. The company’s push towards vertical integration with the entrance into loan servicing in 2010 and title insurance/settlement services through its subsidiary Amrock is another key positive. Not only does it provide a more integrated experience for customers but it also generates margin improvements for the company.” Quote from “Captain Alpha” on Seeking Alpha – “Rocket Companies: Strong Mortgage Play But Valuation Too High” – Seeking Alpha Link

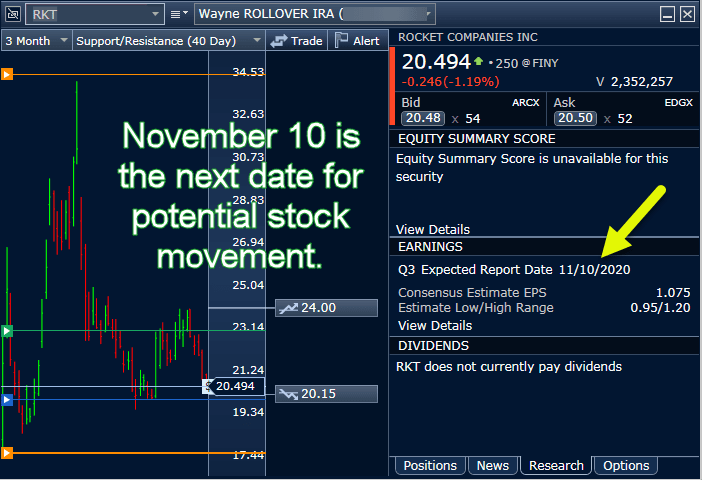

Buy Order with an Expiration Date

When I entered my first order for 100 shares of RKT, I said I was willing to pay $21.60 per share. That order expired a couple of days ago. As it turned out, that was a blessing. Today I saw the price was around $20.50, so I entered a buy limit order for 100 shares at that price. The order filled.

Next Steps

If the price bounces higher after earnings are announced, I will reevaluate my position. I won’t have long to wait, as the Q3 earnings results are scheduled to be announced November 10th. If the price shoots up by 25%, which is possible, I will probably sell the investment. I don’t see RKT as a long-term holding. It is speculative.