Cash Does Not Contribute or Work

Cash is like a lazy teenager (or adult) who sleeps in, eats food like crazy and doesn’t contribute as much as he or she could. There is little energy or work being done, but at least the sluggard isn’t out doing damage to other’s properties and lives. In a similar way, cash is a lazy and “safe” category of wealth. It doesn’t contribute to a person’s income in a low-rate environment. The options for your lazy cash are, sadly, limited. One of the most common questions I have heard this year is, “where can I get some yield for my cash sitting on the sidelines?” The reason this question is asked is that most savings accounts and CD’s are earning essentially nothing for the investor or the saver.

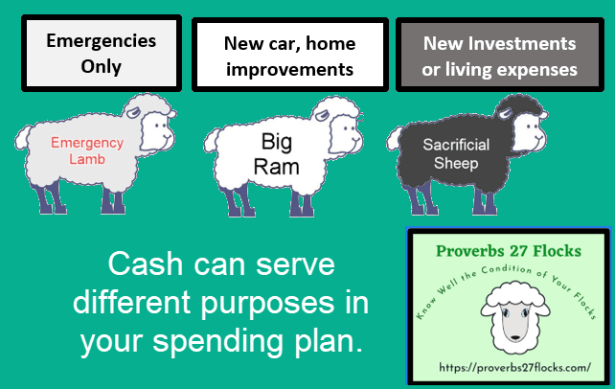

Create Cash Categories

One way to deal with this problem is to think differently. Remember, you don’t have to have all of your money immediately available. It is also prudent to consider if you can accept some risk for portions of your total cash. Cindie and I have cash in each of our four IRA accounts, our three brokerage accounts, in checking, and in two online savings accounts at two different banks. Each cash holding has a different purpose. When I think about cash, I think of it as three different sheep. My emergency sheep, my large expense sheep, and my sheep I might sacrifice in the marketplace.

The Little Emergency Lambs

These lambs are small and tame. It (the cash) stays in the fold so that volatility and risky wolves are unlikely to devour them. Dave Ramsey calls this the emergency fund. In our case, our emergency fund is at Ally Bank, earning 0.60% interest. This savings will only be used in an emergency. Therefore, I don’t fret about the low interest. However, if there is a serious emergency, I don’t have to sell anything to use all or a portion of this cash. ALLY BANK LINK.

The Big Ram Sheep

Big rams are for big jobs. They need to be available, but it is OK if they are in a pasture that is away from the fold. For this portion of our cash, I look at our total non-lamb cash and remember that some of them are about to be sacrificed or might be taken to market in the next six months. For example, we are considering replacing our 2014 Ford Escape with a newer model. We will pay cash for any newer vehicle, so some of the ram cash will have to be sacrificed. Most of this cash is in our Fidelity brokerage, Roth and traditional IRA accounts. It isn’t earning much in SPAXX (SPAXX is the Fidelity Government MONEY MARKET mutual fund.) So it is easy to transfer these sheep to our checking account as needed.

The Sacrificial Sheep

Some sheep have no long-term prospects. I might use them to buy some stocks or some stock ETF’s. About 4% of our assets are in this part of the herd. But while I am waiting for opportunities, I also have incoming dividends that add to the cash fold. Some of that is needed for expenses, as Social Security isn’t sufficient to cover expenses and charitable giving. In addition, some of the “cash” has been invested in two specialized ETFs that have less risk, most of the time, than common stocks have.

The Big Rams: ETFs for Short-Term Purposes

If you need your cash in the next six months, then don’t spend too much time and energy trying to get yield. An argument could be made for putting some of the cash in the ETFs that focus on government bonds, municipal bonds, corporate bonds, or preferred stock ETFs. But the extra time and effort may just be a distraction from your more important marriage, family, work, and church family obligations.

Having said that, if you have $50,000 sitting on the sidelines, and your total retirement assets are $100,000, then you might want to rethink your short-term plans. I couldn’t recommend spending half of your assets on a new car or home improvements unless you have a pressing need that can’t be met by less drastic options.

The Sacrificial Sheep: Alternatives with lower volatility and lower risk

A portion of our “cash” is invested in two rock-solid, low-volatility, income-producing, and reasonably low-risk ETFs. These are NOT growth ETFs. Don’t miss this. You can lose your principal and the value of your shares are likely to stay flat. But you gain some income. The idea is to preserve your cash with as little risk as necessary and gain 3-5% in monthly income or additional cash for future use.

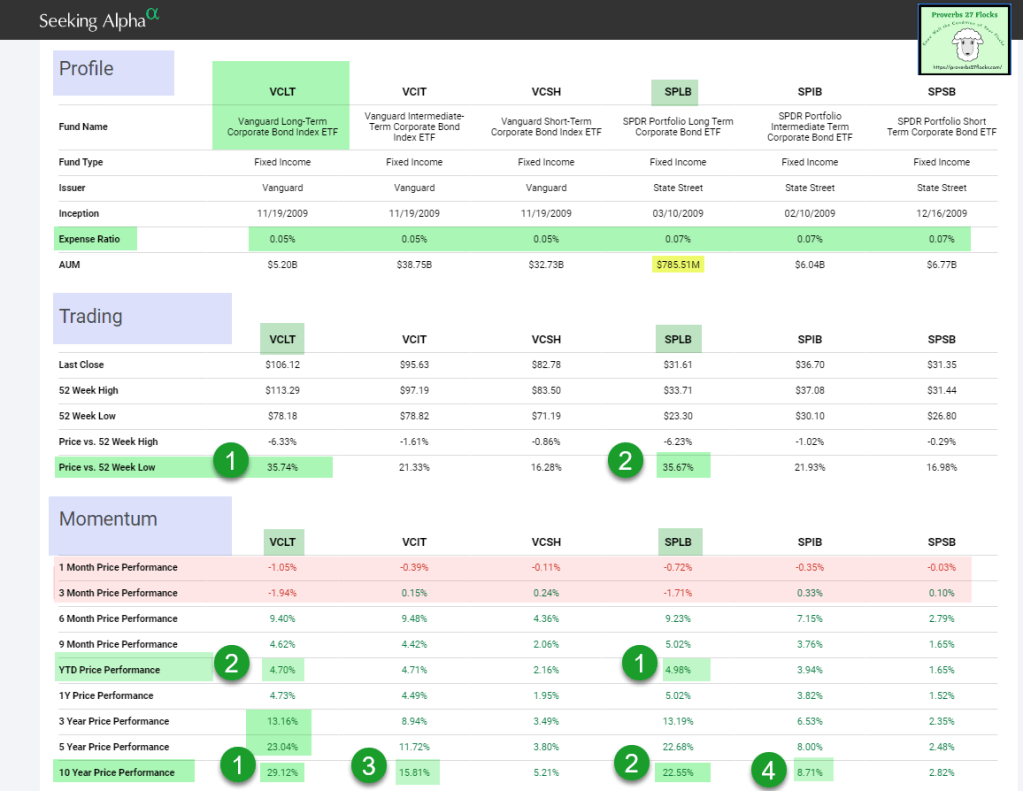

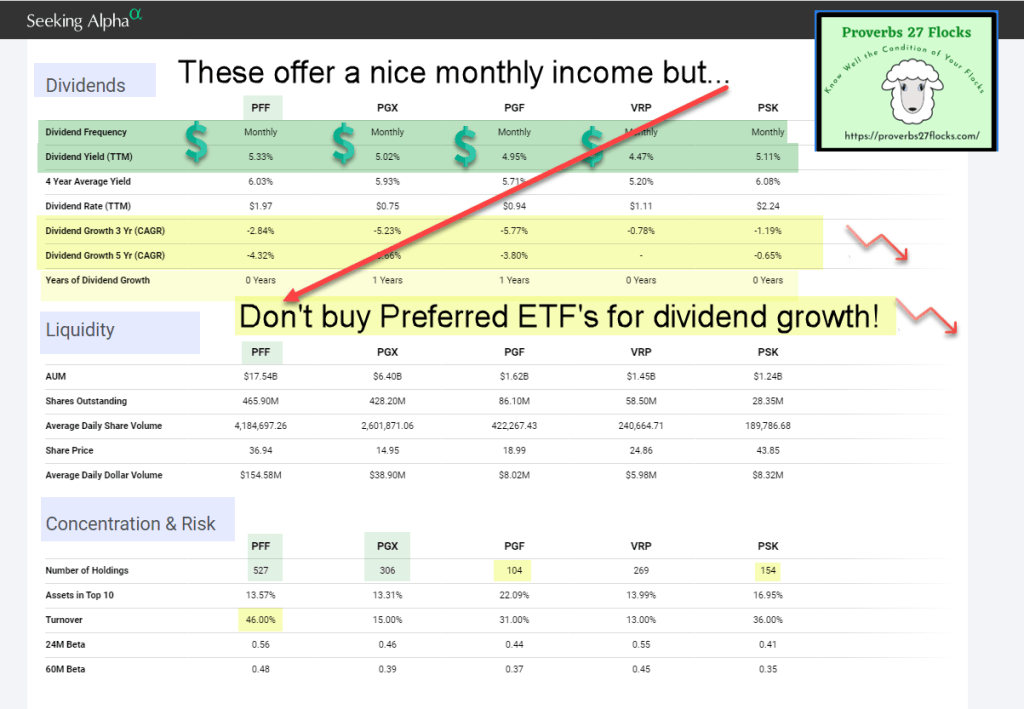

The two ETFs I personally use are VCLT and PFF. VCLT is a Vanguard long-term corporate bond fund. PFF is a highly diversified, preferred stock fund. Think of it this way: when it comes to risk, cash is least likely to lose the principal value, bonds are next in line, preferred stocks follow, then large cap value stocks followed by large cap growth stocks. So, if you don’t want to invest in VYM or DGRO (common stock dividend growth funds), but you want income, consider VCLT and PFF. To help you see these two ETFs in contrast with other similar funds, review the following images.

Summary of the Sheep

Emergency Sheep are kept in a savings account like one provided by Ally Bank. Please don’t think all of your cash dollars have to stay in the savings account fold. But don’t let these sheep wander. See the link below.

Big Rams are kept in a pasture close by. In our case, a portion of the funds in SPAXX fit this role. I can enter and order and these sheep head off into an investment or to pay for some expenses or giving.

Sacrificial Sheep are normally located in ETFs like VCLT and PFF. They are in a pasture having lambs but they aren’t hard to get back and sell.