Suggestions from Ted Bauman’s The Bauman Letter

In the July 2020 edition of The Bauman Letter, Ted Bauman recommended Owl Rock Capital Corp. (ORCC). Because I had never explored ORCC, I decided to do my due diligence to see if this is a BDC (Business Development Company) that fit my overall goals and risk profile. The number of companies that are publicly traded has decreased significantly, reducing the pool of choices. There are many reasons for this, but one of them is that wealthy individuals can buy companies, or portions of them, and keep them private. Others, like Warren Buffett, can swoop in and buy an entire company and make it part of the Berkshire Hathaway stable of companies.

To take advantage of some of this out-of-the-mainstream type of opportunity, I like to invest in BDCs. When a smaller, often private company needs cash to fund growth or other aspects of their business, some BDCs provide loans with attractive income potential for the BDC.

Banyan Investment Newsletters

I believe the annual subscription to The Bauman Letter is $97. I don’t pay that because I have a “life-time” subscription to four Banyan investment newsletters. The other three are “Profits Unlimited”, “Real Wealth Strategist”, and “Total Wealth Insider.” I don’t often buy an investment based on the advice of any of these newsletters, but I do learn some important fundamentals about different companies and types of investments. In this case, after reading Mr. Bauman’s analysis, and doing some research on my own, I bought 200 shares of ORCC.

Ted Bauman’s BDC Criteria with my commentary

Mr. Bauman shared five criteria we should look at when investing in a BDC. They are:

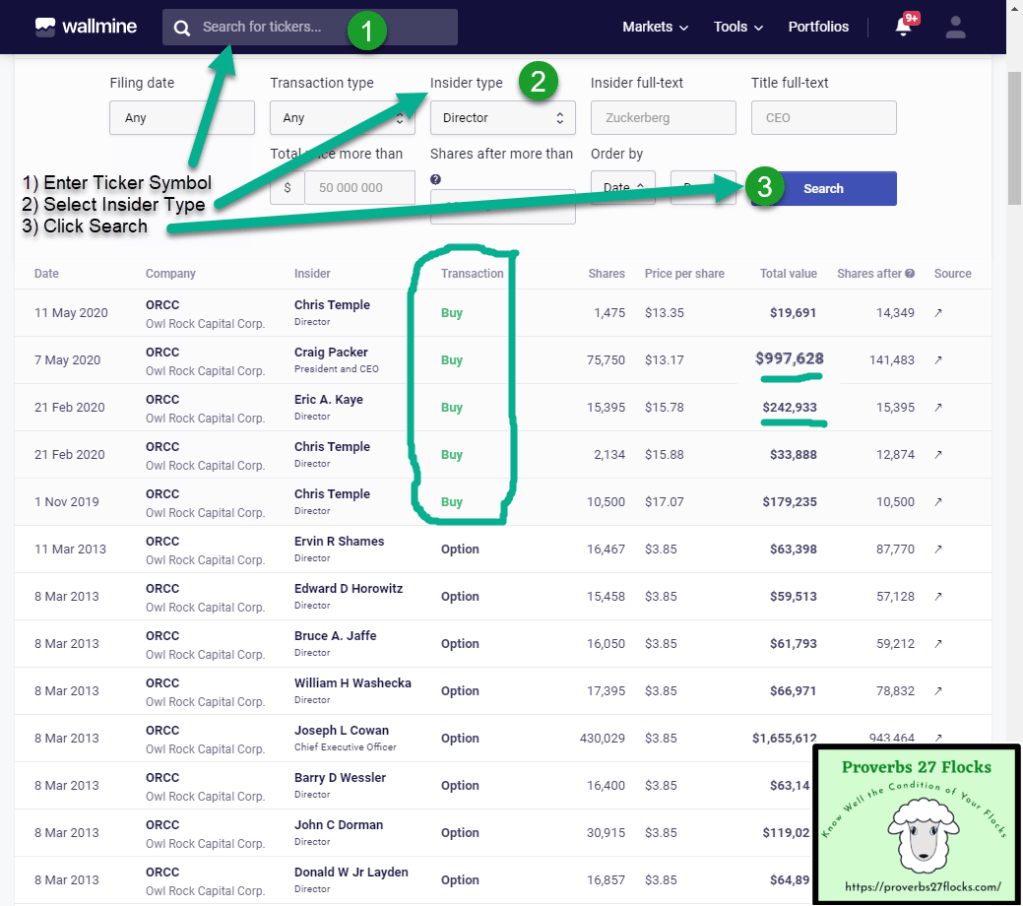

- The BDC should have strong management with a proven track record. ORCC has very capable management with skin in the game. The CEO bought a million dollars of ORCC recently at a price slightly higher than the current price.

- The BDC’s portfolio should be well-diversified across different sectors and balanced between equity and lending activity. ORCC has about 100 companies in their loan portfolio in 27 industries. This reduces their exposure to higher risk by not focusing on a handful of investments.

- The BDC’s loans should be first lien loans and be less than 50% of that company’s asset value. ORCC fits this requirement. In addition, they have never had a loan default due to a bankruptcy of a company in their portfolio. This means they do due diligence in the selection of their loan investments.

- The BDC should use its own equity, not engaging in excessive leveraging. In other words, the debt-to-equity ratio must be sensible and sane. ORCC’s ratio is 0.60 and half of their debt maturities are due 2025 or later. Moody’s rates ORCC as “Investment Grade.”

- The BDC should have investments where other investors have skin in the game as well. ORCC does this by working with companies that have other private equity investors putting their resources in the companies as well.

My Research Included

ORCC’s Dividends

When it comes to dividends, ORCC is unlike many of my investments. First of all, ORCC doesn’t have as long of a track record in paying dividends. Therefore, there are many unknowns about the dividend growth potential. I usually like to see five years or more of dividend history. However, some of the potential in ORCC isn’t just the dividends, but the underlying success of their current investments and future investments. It doesn’t hurt that the current yield is around 10%. That is quite high, and the reason is that the market perceives ORCC as high-risk. I think the market is overly pessimistic, so I bought my first lot of 200 shares of ORCC.

What Price To Pay for Shares?

Another reason I like The Bauman Letter is that Mr. Bauman gives some price-range guidance. Here is a portion of the July 2020 newsletter regarding ORCC:

Risk is a consideration. So don’t buy ORCC or any other BDC’s shares if you are unwilling to weather market volatility. You have to be a bold thinker if you want to experience more growth. But boldness isn’t without risk. Sometimes the profits aren’t endless. That is why I diversify.