Multi-Asset Income Funds

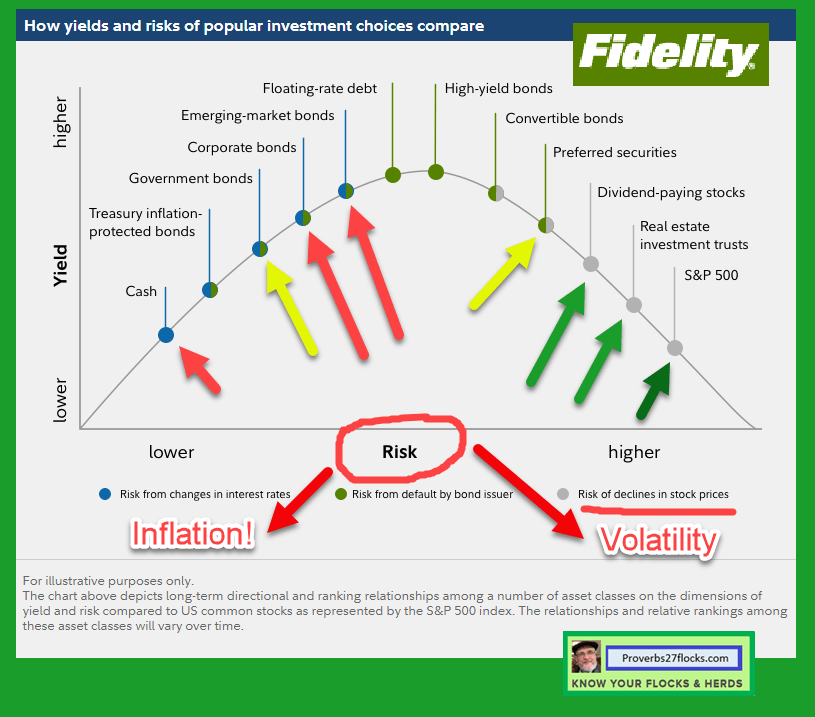

It has been some time since I did a “Friday Fund” review. Yesterday, a Fidelity learning center article caught my attention because I am a “dividend growth investor.” The article’s focus was “income investing” in the 2020 market. One of the funds mentioned, not surprisingly, is a Fidelity mutual fund with the ticker symbol FMSDX. The name for this fund is the Fidelity® Multi-Asset Income Fund. Immediately I was concerned when I saw “Multi-Asset,” but I decided to dig deeper to see if my original gut reaction was warranted. This image helps understand “multi-asset” lingo:

What To Look For

I have a list of things I want to see for any ETF or mutual fund that might enter my portfolio. I want to see: 1) The types of assets in the fund; 2) the expense ratio; 3) the size of the fund in total assets (AUM); 4) the style map (large, mid or small cap; value or growth or blend); 5) the top ten holdings; 6) the turnover rate; 7) the percentage of the investments in stocks, bonds and cash; 8) the regional diversification (US and foreign); 9) dividend growth and dividend yield and 10) number of holdings.

Will I Bash FMSDX?

My purpose isn’t to bash FMSDX, but I want you to be an educated investor. You should have “buy” and “sell” rules for all of your investments and for your overall investment strategy. My frequent readers will probably quickly guess that I am skeptical of all “multi-asset” approaches. This is especially true of target date mutual funds or funds set up with a retirement year like 2035 or 2040. One reason for this skepticism is the heavy weighting given to bonds and cash investments. You don’t and shouldn’t sacrifice long-term portfolio growth on the altar of income. Income, and growing income is very possible without a heavy bond weighting. Of course, you must be willing to endure and, even better, ignore market volatility. You must also pick quality investments.

The Ten Criteria for Mutual Funds or ETFs

If you want to see Fidelity’s own report on this fund, it is stored here: FMSDX File: (2020-07-02_FMSDX-FidelityMulti-Asset Income Fund-31638R717.pdf)

1) The types of assets in the fund – Does it have a weighting in specific sectors or other unique characteristics? No. But with less than 50% equities, that would be a deal killer on its own. To make matters far worse, almost 34% of the assets are “Non-investment grade bonds.” This is not a good sign. The credit quality of 70% of the assets is questionable, rated BBB or lower. Asset class grade is, at best a D. More on this on point number 7.

2) Expense ratio – An expense ratio is like a leak in a balloon. The bigger the hole, the faster the balloon shrinks. I think a leak of 0.10% is acceptable for most decent funds. How does FMSDX measure up? It is awful at 0.85%. Here is another way to do the math. Look at the yield and subtract the expense ratio. If the yield is 3%, that sounds good until you subtract the 0.85%. The fund manager would argue that they are earning their money by picking good investments. I don’t find that to be the case with 95% of the funds I look at, including this one.

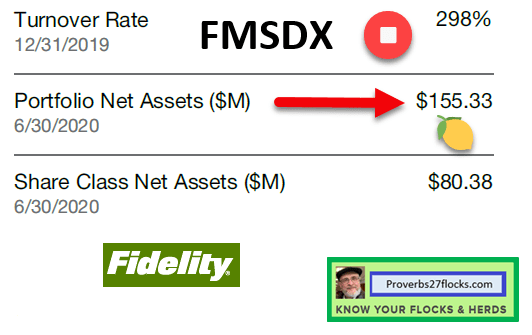

3) Size of the fund in total assets (AUM) – Size matters. AUM is an abbreviation for “Assets Under Management.” That is a fancy way of saying “how big is this fund?” If it has billions of investor dollars, it is popular and probably can be quickly bought and sold due to demand. If it is less popular, it means fewer investors have invested in the fund. This fund, according to Fidelity, has been around for five years. The AUM is RIDICULOUS. Only $155 million is invested in this fund. Trading volume will be disappointing.

4) EQUITY style map (large, mid, or small cap; value or growth or blend) – Of the stocks in this fund, at least they are relatively safe large cap investments. But, like many funds these days, the top positions are AAPL, MSFT and GOOG. Investors need to be aware of the overlap of this fund with other investments, including ETFs and mutual funds they already hold. I’m not impressed, but at least they are following the herd.

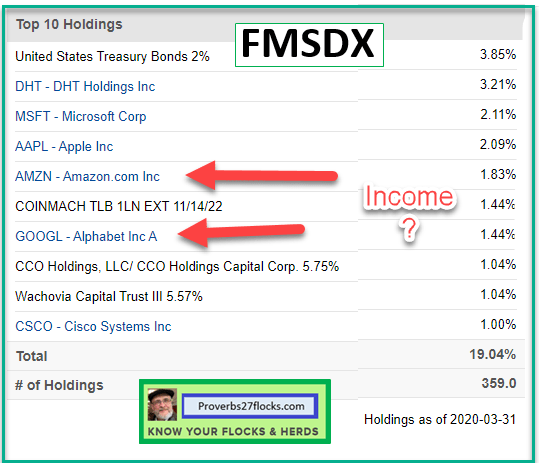

5) Top ten holdings – You can get a good idea of a fund manager’s strategy by looking at where they see opportunities. This fund manager has some interesting picks in the top ten, but as noted in number four, the manager isn’t straying far from the herd. Why pay more for obvious investment picks? Furthermore, some of these aren’t even income plays. For example, AMZN & GOOG don’t pay a dividend. Why am I making a point about this? Because of the name of the fund: it is marketed as an income fund. Income funds should invest in stocks and bonds that throw off income. Be a bit critical of the fund manager’s choices or at least be aware of the marketing department’s role in naming the fund.

6) Turnover rate – turnover rate can be a huge factor for investors. It is true that some of the income can be obtained through capital gains. But that is a higher-risk approach to investing. So if income will be derived from AMZN and GOOG, the only way to get it is to sell some of the shares. The fund manager for FMSDX has a mind-blowing turnover ratio of 298%

7) Percentage of the investments in stocks, bonds, and cash – The types of assets, as shown in the first point, includes stocks and bonds. But the following image adds some more color. Always be somewhat cautious when you see “High-Yield” investments. Depending on what they are, you might find your fund value going down if there are problems with the companies that pay high yield. That is why I prefer dividend growth investments with moderate yields and tend to minimize high yield investments. Also, don’t buy investments you don’t understand. FMSDX has “convertibles.” Do your homework to understand what a convertible is.

8) Regional diversification (US and foreign) – Most of the time I favor US-based investments. However, I also think Canada is reasonably safe. These allocations are not unreasonable.

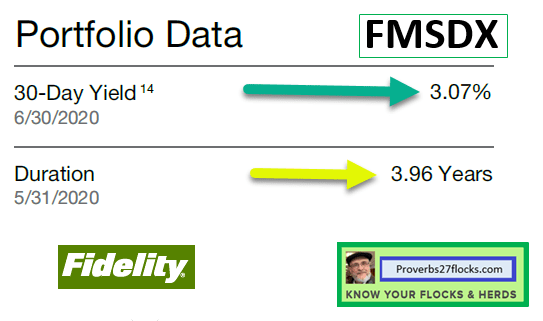

9) Dividend growth and dividend yield and – This fund is relatively new in paying dividends, and it tends to be very up-and-down in this respect. The yield is a respectable 3.07%, but after you subtract expenses it is marginal given the lack of certain dividend growth.

10) Number of holdings – As a general rule, more is better when it comes to funds. Certainly most ETFs should hold at least 100 positions if they aren’t sector-focused. 200-300 provides better coverage. FMSDX is certainly well-diversified in the number of holdings with 358 as of their most recent update.

Fidelity Viewpoints Article

This is the article that recommended FMSDX as a possible choice. They said, “A professionally managed, tactical approach to income investing that can look for opportunities in a wide variety of asset classes may help investors achieve their income goals, despite low rates.” The operative word here is certainly “may.” However, most investors would do far better with a low-cost S&P 500 mutual fund or ETF. These provide good diversification and dividend growth without excessive risk in “high yield” investments. This also helps reduce turnover and keeps the costs from eating away at the dividend yield.

Link to Fidelity’s information about FMSDX: FMSDX

Not sure where you get data… sort of embarrassing how poorly informed this blog post is.

Long bonds beat the US market circa 2000-2020

The S&P 500 underperformed 1 year treasuries for ~40 of the past 90 years. About 1929-1943, 1966-1982, and 2000-2012.

The stock pickers at Standard & Poor’s have a bad habit of buying high and selling low when making changes to their actively managed index. Rob Arnott has written about this extensively. The original S&P 500 stocks from 1957 have outperformed the subsequent index after all the changes, even after all the bankruptcies and mergers, as Jeremy Siegel demonstrated.

In rolling 10 year periods from 1969-2020, the S&P 500 beat MSCI ex-US index only 54% of the time.

High turnover is not unusual for bond funds. BND from Vanguard has a 79% turnover. DODIX has over 94% turnover.

LikeLike

Respectfully, may I suggest that you missed the main point of the post. First of all, I was not suggesting the S&P 500 is the way to invest. Most, if not all of the data was pulled from the Fidelity Investments site on or about the time was posted. This was my review of a specific mutual fund offered by Fidelity and the elements an investor should consider when buying a mutual fund. Bonds, in general, are not a wealth creation engine. Furthermore, please note that my concern had to do with the stocks being held for “income.” Just because a fund has “income” in the fund name doesn’t necessarily make it a good income-generating investment. Finally, I really don’t care what happened in the investing world pre-2000. Historical returns have virtually little or nothing to do with future returns. I fail to see how bonds qualify as a growth engine for most investors.

LikeLike