During a recent training session with a family, I encouraged them to write a goal statement and then pick an investing strategy to achieve that goal. That strategy would then inform their buy and sell decisions. The goal statement I often share as an example says, “Generate a steadily increasing stream of dividends paid by excellent, low-risk companies.”

The Goal Must Be Numbers and Date Driven

A goal is a glorious ideal, but it is generally worthless until you set a numerical, date-driven and remind yourself of the end goal. Therefore, when I wrote my first investment goal statement at age 65, it included the following: “Numerical objective: Grow dividend income to $60,000 in five years when I am 70 years old. Dividends eventually will be withdrawn as RMD’s from the non-ROTH IRA accounts so that income-producing investments will not be sold to fund RMD’s if possible.” This statement, therefore, informed my selection of investments. I wasn’t looking for a 5% yield, just to get yield. I recognized that the increasing balance in my IRA would require increasing earnings if I wanted to avoid selling investments and use most of the withdrawals for purposes not described in my investment goal.

The Goal Is Bigger than Make More Money

Therefore, we also have goals regarding lifestyle (modest), taking care of family and giving to ministries that serve people, build churches (people, not buildings), travel (to help families and friends), and to seek to spread the gospel. We also desire to leave an inheritance to our children. In other words, it isn’t about empire-building or wealth for the sake of wealth. “For what does it profit a man to gain the whole world and forfeit his soul?” Mark 8:36, Jesus

My Goal Statement Lacking Information

The problem with my goal is that it says I wanted the income to reach $60,000 per year without stating what it currently was. If, for example, the current income was $59,000 per year, then in five years to achieve $60K would be an easy goal. Furthermore, for someone with only $5,000 to start investing, setting a goal that is so lofty seems daunting. It is daunting and generally impossible. The goal of the remainder of this post is to scale down the goal based on $5,000 invested today. Don’t lose sight of the fact that your first $5,000 is the most powerful $5,000 you will ever invest. This is something you should realize so as not to be discouraged. The earlier you invest, the better the end result will be.

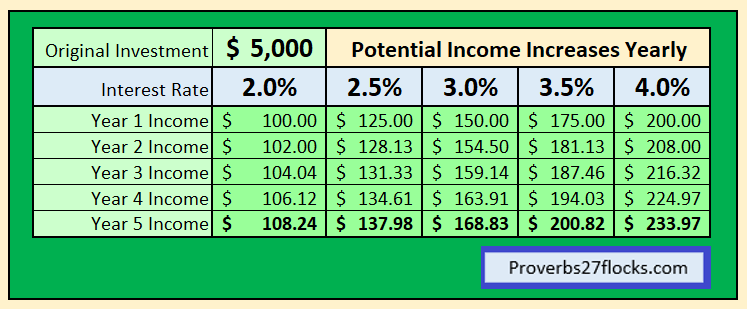

First Example Simple Interest

If I could earn something between 2-4% on the $5,000, and I left the money in a savings account for five years, the power of compounding would make my totals look like this after five years. (This is simplified to assume the interest is only paid at the end of the year. If you receive interest every month, you earn more as the interest compounds.) This assumes the interest rate stays the same for five years. It could go up, but if recent history is any guide, it could go down, down, and more down.

Illustration using annual interest

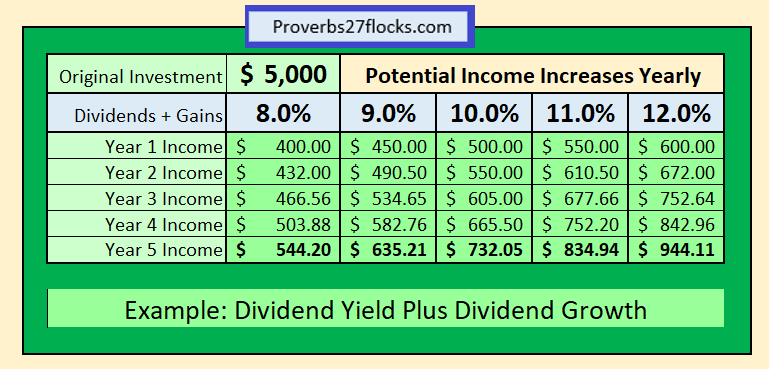

Dividend Yield Plus Dividend Growth

Rather than just a static interest rate of a certain percentage, if we can companies that pay a reasonable dividend yield that increases between 5-10% per year, then our money and income will grow faster, especially if we reinvest the dividends. Most companies pay quarterly dividends. Therefore, the dividends from the first quarter, used to buy more shares or fractions of a share, will earn more dividends in quarter two. Quarter two reinvested dividends will earn even more. If the company raises the dividend by 10% every year, then the fifth quarter (the first quarter of the next year) will result in even more income. Bear in mind that it is also highly likely that your total investment will also grow. In other words, you may have purchased the shares for $10/share five years ago, and they could be worth $13/share at the end of five years. This is in addition to the dividends that you reinvested.

Another Potential Solution

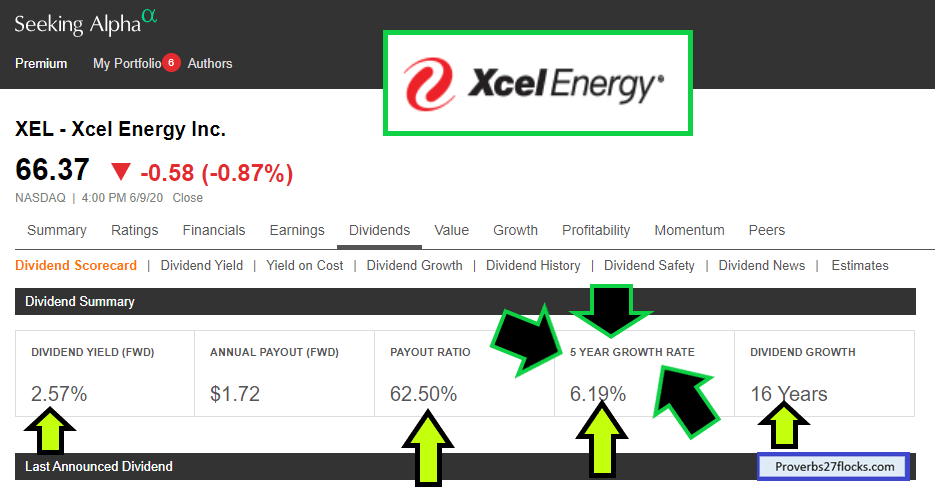

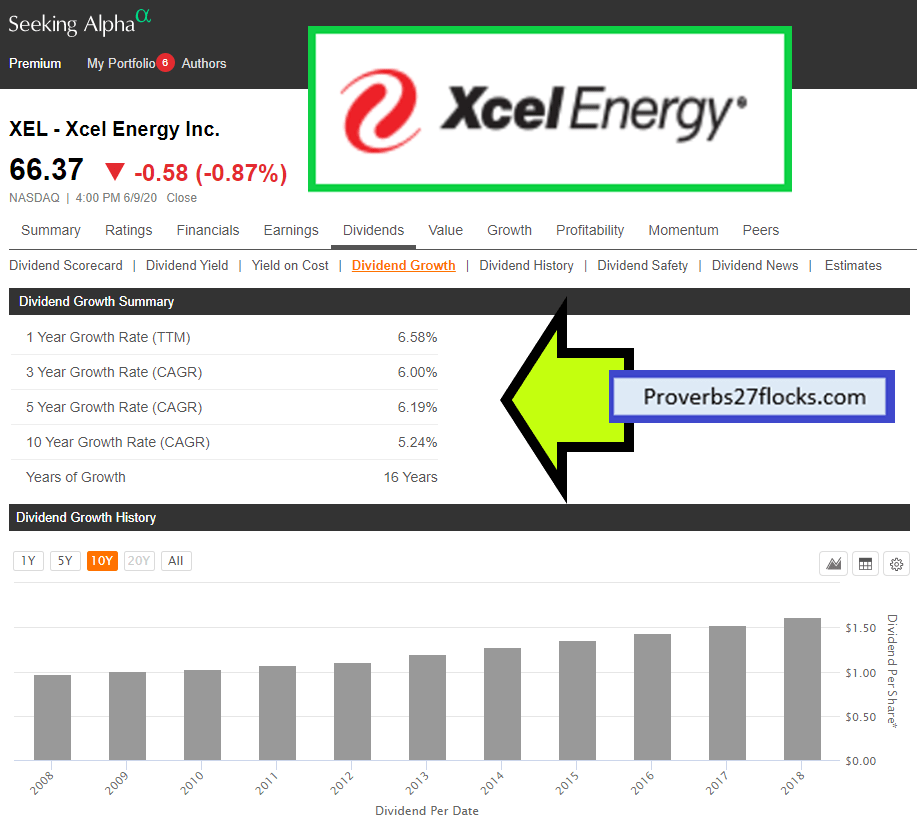

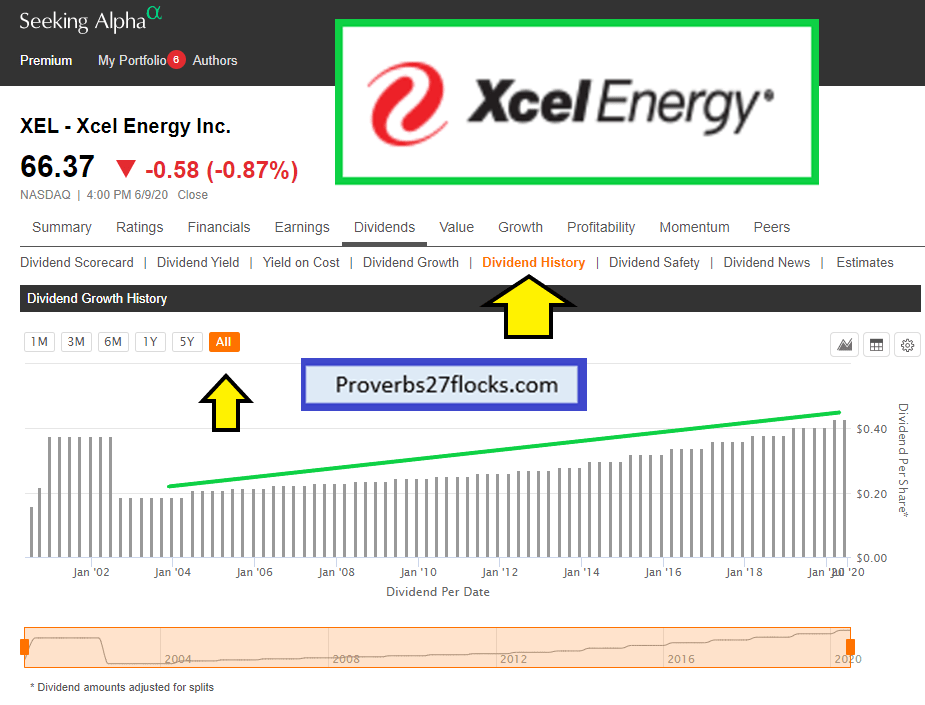

XCEL Energy is One Example

Our investment in XEL is worth 128% more than what I paid for the shares. At the market close today, the price per share was $66.37. My average cost basis for our 603 shares is $29.08. So my original investment of $17,562 is now worth $40,087. But this doesn’t include thirteen years of quarterly dividends. In other words, XEL pays me more today than it did in 2007 and my shares are worth much more now. (I used the dividends from XEL to buy shares of other companies. I did not automatically reinvest the dividends in XEL.)

The Bottom Line

Set your goal based on a realistic expectation of the growth you can expect. I think 5-10% dividend growth is easily achieved. If you start with a yield of 2.0%, you will find your income is considerable after five years and even more after 13 years.