Why Have A Savings Account?

There are good reasons a savings account is a wise choice for some of your money. Many people have no savings, and when bad things happen, they borrow money from a bank and pay the loan back with interest. Many also just keep using their credit cards and wind up deeper-and-deeper in debt. Some of the reasons for a savings account include planned and unplanned expenses.

Prepare for Planned and Unplanned Costs

- Emergency Fund

- Saving money for annual expenses like home or auto insurance.

- Setting aside some money for a vacation or for Christmas gifts.

- Saving for a major purchase, like a car, college or a new roof on your home.

Where to store money for these things?

For these things, seek to keep savings: Safe, Liquid, Insured & earning Interest

Savings accounts are “safe” because they also include insurance from the Federal Deposit Insurance Corporation (FDIC). Some brokerage firms, like Fidelity Investments, offer cash management accounts, which automatically move cash in their clients’ accounts into bank savings accounts which provide them with FDIC protection.

Another benefit of a savings account is that they are liquid. That means you can access your savings when you need or want to. You don’t have to sell an investment to get cash for a purchase.

FDIC Insurance is a benefit of a savings account. This means the government insures you against losing your money if your bank fails or goes bankrupt. The insurance covers losses of up to $250,000 per person, per bank, per account ownership. That limit may require you to spread your money across accounts at several banks in order to make sure all your money is insured. Unfortunately, savings accounts are a poor investment. That is because they don’t pay much interest and inflation usually grows faster than the interest earned.

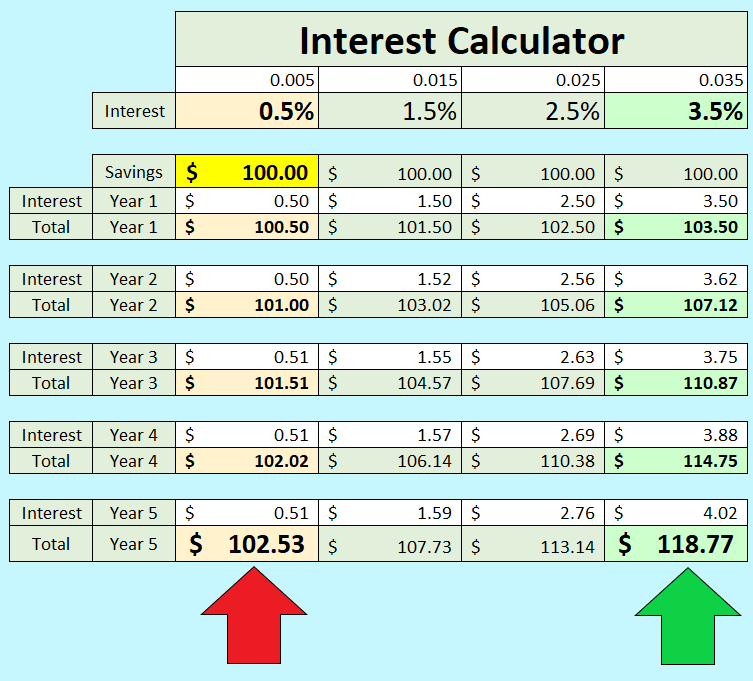

Each saver should be thoughtful about how much she or he saves in a savings account and look for ways to earn more on the money as it grows. The following “Interest Calculator” illustrates the power of compounding interest. Compound interest is interest on your total, including the growing interest earned. If the interest is small, your money doesn’t really grow much. If you have $100 and you receive 0.5% interest, at the end of five years you will have $102.53. But if you can invest your $100 at 3.5% interest, you will have $118.77. That might be enough to break even with inflation.

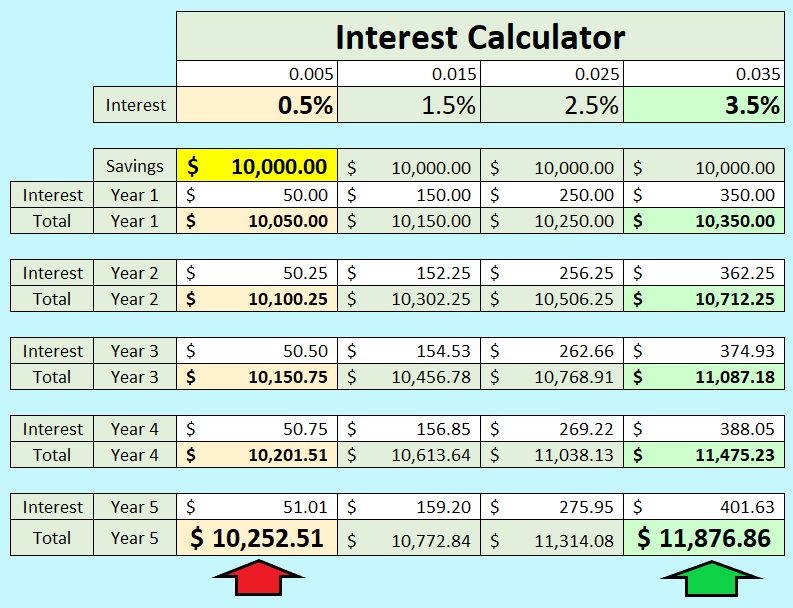

The difference becomes even more apparent if you have $10,000 in savings. You would gain $252.51 at 0.5% but $1,187.86 if you earned 3.5%.

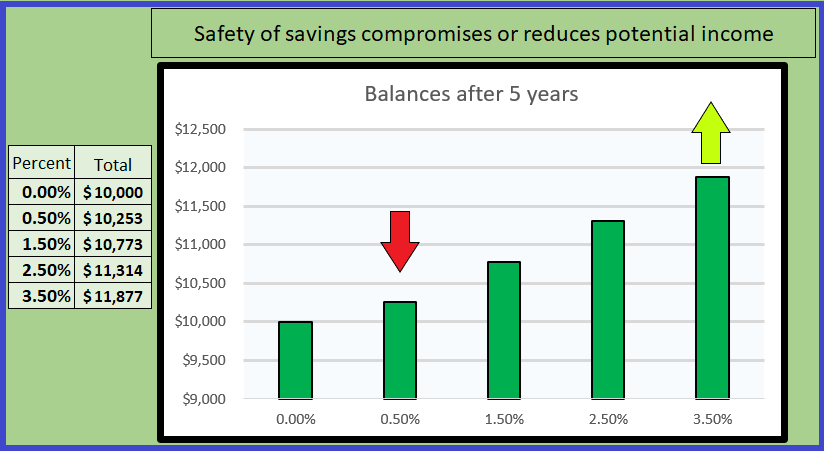

Sometimes it is easier to see a picture to show this than a bunch of numbers. Here is what it looks like with a bar graph.

What Makes Savings & CDs Poor Investments?

It probably isn’t wise to call a savings account an investment. Your dollars are not going to grow very fast. You probably won’t even keep up with inflation. As a result, you might have to use more dollars to buy something after five years that cost less when you first saved $100.

Investments should be able to return more to the patient and careful investor. It isn’t unreasonable to expect an 8% return or even more. If you invest $10,000 at 8%, you would probably have over $14,500 in your account after five years. But where can you get an 8% return?

One way is to own small pieces of growing businesses. This is done by buying shares of stock in a company like McDonald’s or Apple or Disney. The stock can pay the investor in two ways. Many companies pay a dividend. A dividend is money the company pays you because you own a part of the company. The other way is in the growth of the value of the shares. If you buy a share today for $100, it could be worth $125 in a couple of years. Unfortunately, it could also be worth less than $100. Even so, there are ways to avoid losing a lot of money. We will talk about that in a future lesson.

Fidelity Investments had a Viewpoints training article that offers a good summary of several ways you can handle cash. Their list includes savings accounts, money market mutual funds (Examples include: FDRXX, SPAXX), Certificates of Deposit (CDs), short-duration bonds and short-duration bond funds. The simplest and easiest solution is an online savings account at a bank like Ally.

FIDELITY INVESTMENTS: Viewpoint Article

This is a link to Ally Bank: ALLYBANK

You can also download an Excel spreadsheet I created and saved. If you download the spreadsheet you can change the dollar amount in the yellow box to any number you want to use and all of the other numbers will recalculate automatically.

Link to the Investment Calculator Spreadsheet: EXCEL SPREADSHEET