Your Budget Reveals Your Priorities

To create a good budget, you should include all income, spending, saving, giving and investing. But don’t miss the hidden costs of life and little pleasures like a Culver’s sundae or a Pepsi. Far too often a family or personal budget is not complete because we don’t consider all costs and all spending. We tend to spend money and then wonder where it went. This is especially true with home ownership and the purchase or lease of any vehicle. But it is also the “little” things. Let’s start with an example that has many hidden and forgotten costs.

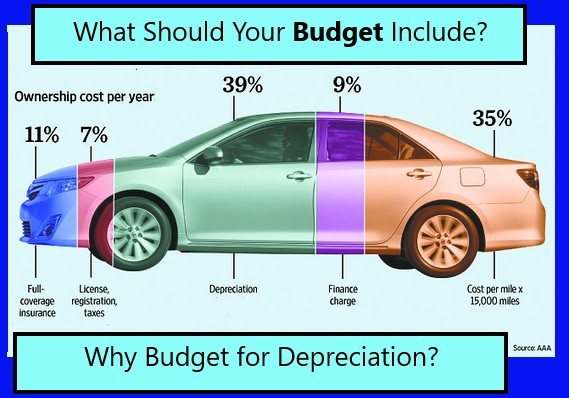

Buying a Car – What should we remember?

Let’s say I plan to buy a car that costs $10,000.

- 1) How will I budget for this purchase?

- 2) What does it really cost to take possession and drive it home?

- 3) What will it cost to own it and use it?

- 4) How long will it last?

If you want to reduce your costs, don’t forget rule number one: Pay for the car with cash. Avoid loans, because they add to the cost. If you get a loan you will pay monthly. Sadly, when most finish their last payment, the vehicle won’t be worth what you paid for it. And don’t be deceived by zero percent interest. Rather, see if you can negotiate for a better purchase price. The following are the common costs that many pay but they don’t always have in their budget.

- Monthly: Repaying a loan from a bank or the car dealer.

- Semiannual: Liability and comprehensive/collision insurance.

- Monthly: Paying for fuel.

- Annual: Maintenance: Oil changes, tires, brakes, batteries and ?

- Annual: License Plates

- Various: Driver’s license, paying for tolls, parking & car washes.

Depreciation and Inflation

When it is time to buy the next car, what will you do? The cost we often miss is called “Depreciation.” This is a fancy way of saying that the car we paid $10,000 for is worth much less the next year and every year thereafter. This is because you are adding miles to the car, and miles wear out parts. Most cars have a useful life of about 10-15 years unless you are a mechanic or drive in a way that reduces wear and tear. Ten years from now you might not even be able to get $1,000 for your car. And guess what? You will probably have to pay more than $10,000 to get a similar car ten years from now due to inflation. (See the video at this link.)

A budget should show income.

Income: List all sources of money you receive in a month or at various times during the year including estimated dollar amounts. This can include paychecks, tips, sales commissions, savings account interest, investment income like dividends, and maybe even gifts.

Fixed and Discretionary Spending

Expenses: List every purchase you make in a month, split into two categories. They are fixed expenses and discretionary spending. If you can’t remember where you’re spending money, review your bank statements, credit card statements, and brokerage account statements. You should total all expenses every month and see how they align with your budget. If they don’t your budget needs review.

Fixed expenses: These are the purchases you must make every month, and whose amounts don’t change much, and are considered essential. This includes food, gasoline, rent/mortgage payments, loan payments, and utilities like gas, electric, water, internet and phone services.

Discretionary spending: These are the non-essential, or purchases you make on things like toys, McDonald’s, jewelry, extra shoes, designer clothing and travel for fun. These are “wants” and shouldn’t be called “needs”.

Building an Owner-focused Budget

As you build your budget, remember God is the owner of every dollar you receive. Haggai 2:8 “The silver is mine, and the gold is mine, declares the Lord of hosts.”

Think about how God would be pleased with the way you spend and give and save. Here are some important scriptures to guide your thinking:

PLAN CAREFULLY: God doesn’t admire sloppiness or laziness. Proverbs 21:5 “The plans of the diligent lead surely to abundance, but everyone who is hasty comes only to poverty.”

THINK MINISTRY: Does your budget care for those who have the work of preaching and teaching? Malachi 3:10 “Bring the full tithe into the storehouse, that there may be food in my house. And thereby put me to the test, says the Lord of hosts, if I will not open the windows of heaven for you and pour down for you a blessing until there is no more need.” 2 Corinthians 9:7 “Each one must give as he has decided in his heart, not reluctantly or under compulsion, for God loves a cheerful giver.”

BE GENEROUS: Does your budget reflect God’s generosity towards you? 2 Corinthians 9:6 The point is this: whoever sows sparingly will also reap sparingly, and whoever sows bountifully will also reap bountifully.” Proverbs 14:31 “Whoever oppresses a poor man insults his Maker, but he who is generous to the needy honors him.”

BE CONTENT: Does your budget reflect contentment? Hebrews 13:5 “Keep your life free from love of money, and be content with what you have, for he has said, ‘I will never leave you nor forsake you.’” Luke 12:15 “And he said to them, ‘Take care, and be on your guard against all covetousness, for one’s life does not consist in the abundance of his possessions.’”

EXERCISE SELF-CONTROL: You don’t need everything on your want list. Set proper priorities. Proverbs 25:28 “A man without self-control is like a city broken into and left without walls.” Proverbs 24:27 “Prepare your work outside; get everything ready for yourself in the field, and after that build your house.”

THINK ABOUT FAMILY FIRST: God expects us to care for our mothers, fathers, children and other family members. This might mean you need life insurance if you are the one who provides income for your family. 1 Timothy 5:8 “But if anyone does not provide for his relatives, and especially for members of his household, he has denied the faith and is worse than an unbeliever.”

LIFESTYLE: BE MINDFUL ABOUT THE OWNER: If you think properly, you won’t have riches for self-indulgent luxuries as a priority. Luxuries don’t last. Does your budget reflect that reality? James 5:1-5 “Come now, you rich, weep and howl for the miseries that are coming upon you. Your riches have rotted, and your garments are moth-eaten. Your gold and silver have corroded, and their corrosion will be evidence against you and will eat your flesh like fire. You have laid up treasure in the last days. Behold, the wages of the laborers who mowed your fields, which you kept back by fraud, are crying out against you, and the cries of the harvesters have reached the ears of the Lord of hosts. You have lived on the earth in luxury and in self-indulgence. You have fattened your hearts in a day of slaughter.”

SAVE AND INVEST THOUGHTFULLY: Getting rich quick is a quick way to be poor. Proverbs 13:11 “Wealth gained hastily will dwindle, but whoever gathers little by little will increase it.”

REMEMBER YOUR BRIEF OPPORTUNITY: You don’t have unlimited days to make a difference. James 4:13-14 “Come now, you who say, “Today or tomorrow we will go into such and such a town and spend a year there and trade and make a profit”— yet you do not know what tomorrow will bring. What is your life? For you are a mist that appears for a little time and then vanishes.” We ought to say that our budget is as follows, “if the Lord wills.” James 4:15

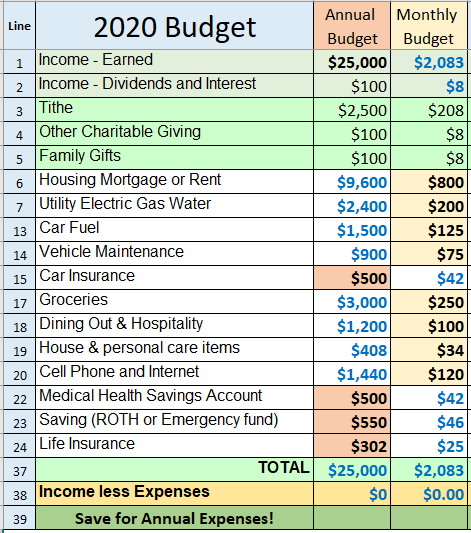

What does a Simple Budget Look Like?

Here is a simple budget that includes income, tithing, giving, housing, transportation, food, insurance and investing.

Here is one of many good resources for creating a budget: Dave Ramsey