Know the P/FFO and ignore P/E

In January I wrote an informational post about REIT investing. REITs are “Real Estate Investment Trusts.” I reviewed some important criteria for evaluating a REIT investment. This included checking the REITRATING at Reitnotes.com and looking at the payout ratio based on Funds from Operations (FFO). I mentioned that I used Weiss Ratings at that time, but if you have been following my blog posts, you know that I discontinued that subscription. It isn’t needed for this analysis.

Recently I read one of the investment newsletters I receive from Banyan Hill. The one I saw was a weekly edition called “The BAUMAN LETTER”, written by Ted Bauman. Of the four Banyan Hill newsletters I receive, I think his offers the best ideas and advice. In this update, he talked about Crown Castle International Corp. (NYSE: CCI).

He discussed buying it in tranches. A tranche is a French word that means a “slice” or a “portion.” If you have a cherry pie, you don’t eat the whole pie at once, you eat a slice. If you are buying an investment, it often makes sense to buy it in smaller slices. Therefore, if your goal is to buy 100 shares, you might buy 25 shares this month, 25 the next and so on until you have 100 shares. I set a target of at least 100 shares and bought my first 25 shares in October 2019. I added shares on October 31st and bought four different times in November. Some of my purchases were for 25 shares, some for 15 shares and some for 10 shares. Because of the prices I paid, my average cost is $133.54 per share, even though 25 shares I purchased on October 31, 2019 were $138.51 per share. By being patient and methodical, I was able to establish my position in tranches and keep my cost low. CCI last traded on Friday at $155.09 per share, and given the recent market volatility, I am pleased.

CCI is a REIT. You probably use what CCI owns. It invests in cell phone towers and fiber-optic networks. When it comes to dividends, the lower your cost basis, the higher your eventual yield on cost will be. If I expect a company’s stock price to fall, as was the case when I bought CCI, it makes sense to buy chunks of it over time as the price falls to lower our cost basis.

Whenever you see a company’s dividend yield, it’s expressed as the last four dividend payments as a percentage of the company’s current price. Once you bought a dividend income stock, one thing that matters is your dividend payment relative to what you paid for the company. That is known as the yield on cost. When I buy more of a dividend paying stock as its price drops, my yield on cost increases. That is one of the reasons I buy when there is a market panic. I get more shares at a lower price, giving me better potential for long-term earnings.

Some of Mr. Bauman’s readers wrote to tell him that they weren’t going to buy CCI because they thought CCI’s price earnings (P/E) ratio was excessive. They found what they thought was a better story in REIT American Tower Corporation (Ticker: AMT). Mr. Bauman said “That’s a mistake. And it’s based on a common misunderstanding. You see, when most financial websites present data, they default to the P/E ratio as the measure of a company’s earnings.”

For REITs the traditional price earnings (P/E) ratio isn’t the correct measure to assess earnings. REITs have characteristics that distort earnings. The better measurement for a REIT is P/FFO. This is the price over Funds from Operations. Funds from Operations is the same measure you use when looking at the dividend payout ratio for a REIT. If you use earnings, you will see a dividend payout ratio that should normally scare you away from an investment. In other words, the dividend payout is often greater than “earnings” but less than “funds from operations.”

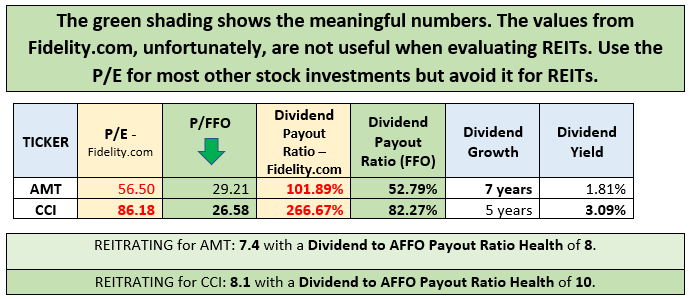

If we compare the P/E and the P/FFO for CCI and AMT we see the following. Both have awful P/E ratios, but AMT looks better to the uninformed. There are aspects of AMT that make it attractive. It has a longer history of dividend growth and a lower dividend payout ratio using FFO. But from a P/FFO standpoint I like CCI better and I like a higher payout ratio and higher dividend yield. In addition, CCI has a better REITNOTES score. AMT’s Debt Leverage Health is scary.

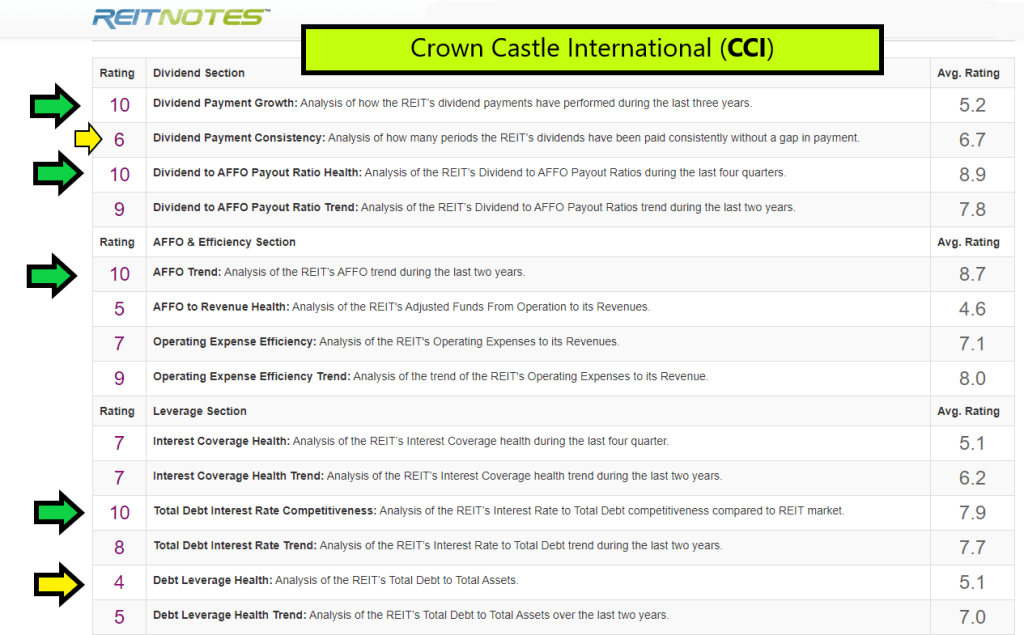

Note the following characteristics from REITNOTES web site for CCI and AMT: