Rule No. 2 for Selling an Investment – Five Percent

No investment is risk-free. All investments have risk. This includes cash, CD’s, bonds, stocks, real estate, gold coins, art collections and baseball cards. To be clear, I don’t consider baseball cards as a very good risk/reward proposition. But there is another risk most understand. It is the risk of putting all your available cash into a single investment. Risk is also heightened when you have a small number of investments and one of them is much larger than the others. For example, if I have $100 and invest the dollars evenly in ten different companies, I am facing $10 of potential loss if any one of them declares bankruptcy. The reality is that you are risking 10% of your total capital in each company, believing they will be profitable and grow your ten dollars. Is that wise?

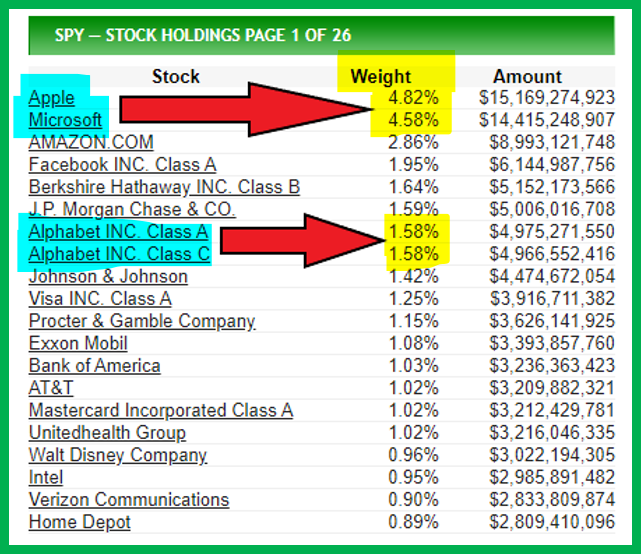

Most investors like mutual funds and low-cost ETF investments because they often invest in many companies. But don’t assume you are getting equal pieces of 500 companies if you invest $500. For example, ETF SPY (SPDR® S&P 500 ETF Trust) holds 506 companies. If you invested $506 in this fund, you don’t have a dollar invested in each company. You would have about $24.39 invested in Apple and $23.17 in Microsoft. The top two companies are almost one-tenth of your total invested dollars. You would also own a portion of eBay. But your total investment in eBay would be $0.50. If you own three different funds, and all of them have AAPL and MSFT in their list of investments, you will own more of Apple and Microsoft than you might want to have. Also notice in this illustration that SPY really holds 3.16% or $16/share of Google (Alphabet Class A and C) shares. In addition, realize SPY has quite an investment in technology companies. At least seven of the top 20 investments are technology-focused investments. SPY is diversified, and it is a credible investment, but be thoughtful if you buy it and other mutual funds or ETFs.

What is the second rule?

Over time, even if you carefully selected a broad mix of funds or individual stocks, it is likely several of them will eventually represent a much larger portion of your total invested dollars. Therefore, my rule is that I will never exceed more than 5% of my total invested dollars in a single company’s stock. So, if the value of an investment goes up faster than the other investments, I will often sell a portion to lock in profits and to avoid having too many eggs in one basket. Recently I sold some of Cindie’s mom’s shares of AAPL for that very reason. Her shares grew so much in value that it was time to sell. Her AAPL holdings are now at 4%. I also sold my shares of NEE and AAPL this year to reinvest the dollars for more diversification.

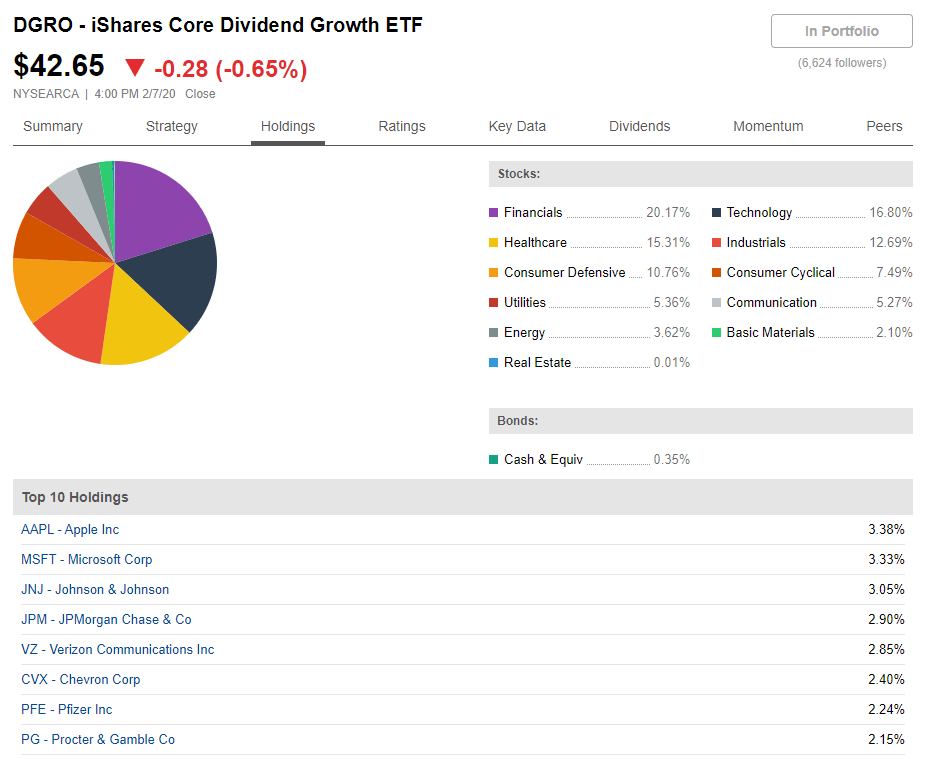

If you own shares of a mutual fund or ETF, it is tempting to ignore them and just let them grow. However, even here there is room for change. I started buying ETFs for our grandchildren in 2015. One of those ETFs is FTEC – Fidelity® MSCI Information Technology Index ETF. The 3-year and 5-year returns have been amazing. As a result, the FTEC investment was much bigger slice of the total holdings. The dollars invested in technology companies was too great when compared to the whole. I sold some of their FTEC shares and bought more shares of DGRO, increasing their exposure to many other companies and to more business sectors and reducing their heightened exposure to technology.

In summary, you should understand the top holdings in your mutual funds and ETFs. You can inadvertently have too many dollars invested in Apple or Microsoft. If you buy individual stocks, and one of them does extremely well, it might be wise to sell a portion and buy another good investment. My rule is 5%. You might want to have a similar rule.

As a buy-and-hold dividend-growth investor I am never in a hurry to exit a quality investment. But I also don’t want to face an ugly surprise if a stock suddenly drops because of bad news. Think Boeing 737 Max. Boeing’s stock has been severely punished by the market. (Thankfully, I sold my mother-in-law’s BA shares before the news got bad.) Big good companies can fail. Remember Sears? Boston Store? Toys R Us? Kodak? Enron? General Motors? Don’t think it cannot happen to your investments.

Don’t forget rule number one! Here it is: https://proverbs27flocks.com/2020/02/07/selling-investments-rule-no-1/

Dear Mr. Winquist, I want to make sure I understand rule #2 and learn from an experienced investor. By the way, I love your blogs, God bless. I bought 80 shs of MSFT in 2014 for 46.60/sh. And since then I have purchased a few shares here and there totaling 105shs with a cost basis of 78.19. It is now 9% of my taxable portfolio. I have an IRA but am not including it or should I? That would be my question #1. If that is the case then MSFT would represent 5.5% of my total portfolio, which includes a brokerage account, IRA, ROTH and HSA with Fidelity. Either case I would need to trim. Do I trim from my highest cost basis or lowest cost basis. To get it below 5% I would need to trim from my lowest cost basis. Am I on the right track? Thoughts, lessons, I am all ears or in this case, eyes. Thank you for your time.

LikeLiked by 1 person

You asked a great question. I believe it is best to include all of your accounts when you determine the weightings. Therefore, while MSFT might be 9% in a single account, it really isn’t quite that overweight when you look at your entire portfolio. Also, I don’t view MSFT has a high risk investment. It is likely to continue to move higher because of the business model and cloud opportunities.

The only reason you care about cost basis, in my opinion, is related to taxes. If you sell the shares with the $46.60 cost per share, your capital gains will be greater than if you sell the other 25 shares. I generally use LIFO for my selling in both my taxable and non-taxable accounts. This can be set at the account level as a default. LIFO is “last in first out.” FIFO is first in first out. Other than taxes, I’m not certain it really matters much which approach you take.

Having said all that 5.5% doesn’t seem like a warning alarm to me. If it was 7-10% I would be more likely to lighten up. The other question you must ask yourself is “what will I buy to replace this investment?” Is there another opportunity that gives you better long-term growth?

Hope this helps. Thanks for the kind words! Wayne

LikeLike