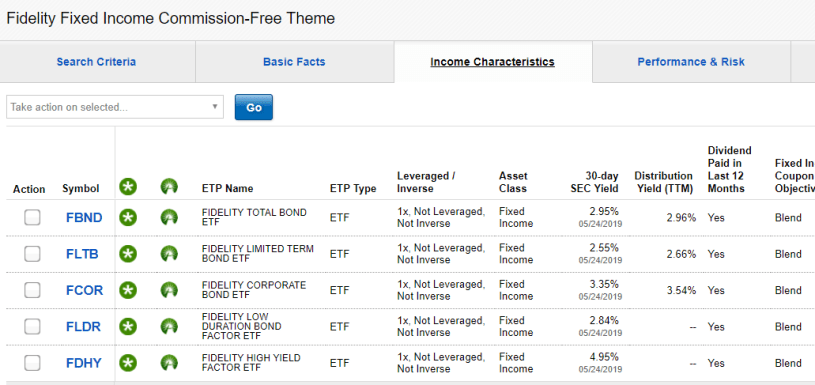

Fidelity’s ETF offerings are good. If I must choose between investing in Certificates of Deposit (CD’s) and a good bond-focused ETF, I will usually pick the bond ETF over the CD. Fidelity has many choices, including iShares ETFs, but they also have five ETFs that can provide fixed income. The ETF’s expense ratio does eat away at returns, but the expense ratio for Fidelity’s five is reasonable.

The nice thing about a bond ETF over a CD is that you can sell the ETF when or if you want additional cash. It is generally best to wait until the CD matures to get your investment back. Of course, the risk with the bond ETF is that it can be worth less (or more) than what you paid for it. With FDIC-insured CD’s there is little risk to your original investment. If you bought a $1,000 CD with a 12-month term, it is worth $1,000 in twelve months. Be careful to compare rates. You might do better with a good CD.

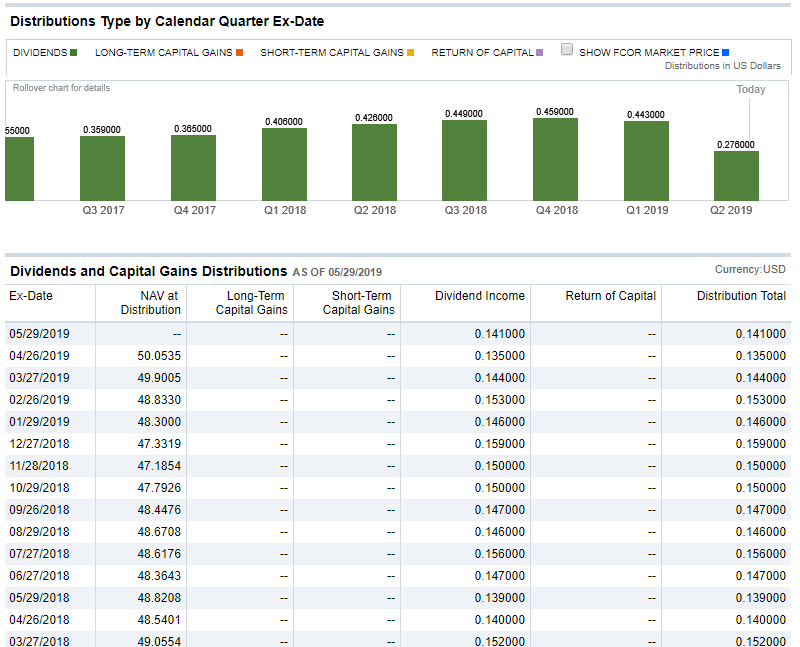

In addition to losing value, the bond ETF can also have varying income. One of the five, FCOR, has income that varies as shown in the following illustration. You will find this to be true of most, if not all bond ETFs.

For the most part, I still prefer stocks and stock ETFs. I want both growing dividend income and the potential for much greater gains in the total investment value. VYM or SCHD are good ETFs for that approach.

Link to Fidelity’s Income ETFs: https://research2.fidelity.com/pi/etf-screener#theme/510