Today’s blog post will be more general in nature. Those of you who know me, know I am not a big fan of bonds. That is an understatement. However, that does not mean that I totally ignore bonds or bond ETFs or avoid them. But I keep less than 5% of our investment assets in cash, bond ETFs and individual bonds. At age 68, my approach is often viewed as ‘very aggressive’ or VERY risky!

I beg to differ. Bonds are “safe” but won’t often grow in value and the percentage paid on the investment isn’t likely to grow. You are more-or-less in a lose-lose situation. The one redeeming quality is the steady income stream.

Fidelity suggests that if you are interested in exploring bond ETFs, that you check out the list of the largest bond ETFs by NAV within 8 bond fund categories. Fidelity offers five other bond ETFs that are available for purchase on Fidelity.com commission-free: Fidelity Total Bond ETF (FBND), Fidelity Corporate Bond ETF (FCOR), Fidelity Limited Term Bond ETF (FLTB), Fidelity High Yield Factor ETF (FDHY), and Fidelity Low Duration Bond Factor ETF (FLDR). Let’s just say the Weiss Ratings on all five of these is poor or awful.

When it comes to the bond market, you have many possible choices. You could build a diversified portfolio of individual bonds but that is a huge task. Bond mutual funds and bond ETFs are often a low-cost way to buy a diversified basket of bonds, but be careful!

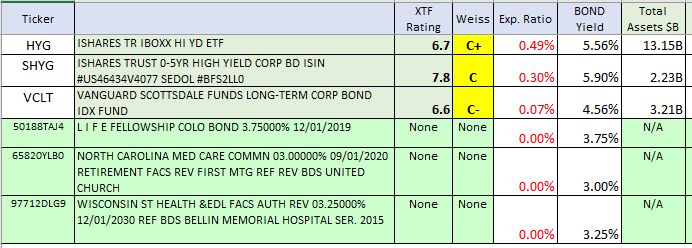

Bond mutual funds generally provide monthly holdings disclosures and discourage short-term trading of fund shares. Bond ETFs are required to disclose their holdings daily to support daily exchange trading activity. Here are the bonds we currently own. Notice that three of them are individual bonds and all of them are held in a taxable account. There is a tax advantage for two of the three. One is a church, and there is no tax advantage for that bond. I am not recommending HYG, SHYG or VCLT, but they aren’t bad. Don’t forget to subtract the expense ratio from the bond yield.

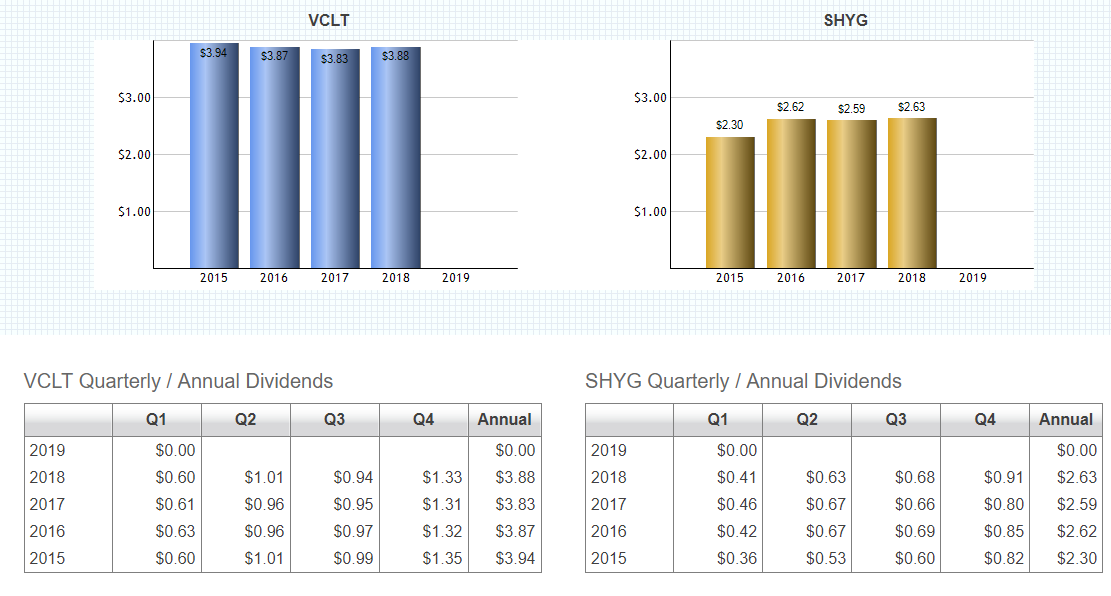

For VCLT and SHYG: Notice that income is NOT increasing from these investments! Don’t buy a bond if you want increasing income over time.

LINK: https://www.fidelity.com/viewpoints/active-investor/bond-etfs