The last of five risks in this series is called “Interest Rate Risk.”

Thus far we have talked about opportunity risk, reinvestment risk, inflation risk and benchmark risk. This final risk factor is one that I see all to often. In an effort to be “safe” the overly-cautious investor actually assumes a higher level of risk. Interest rate risk combined with inflation risk is a killer combination. You actually wind up losing instead of maintaining or saving.

In a misguided but well-meaning effort to preserve their assets, many become fearful of market volatility and shift heavily to bonds, CD’s and cash. When interest rates rise, bonds lose value. If you sell a bond before it matures, you can experience significant loses. But even if you hold the bonds to maturity, you have entered a high-risk environment. If you can steel yourself for market volatility, and remember volatility does not necessarily equal risk, you will realize better long-term investment returns.

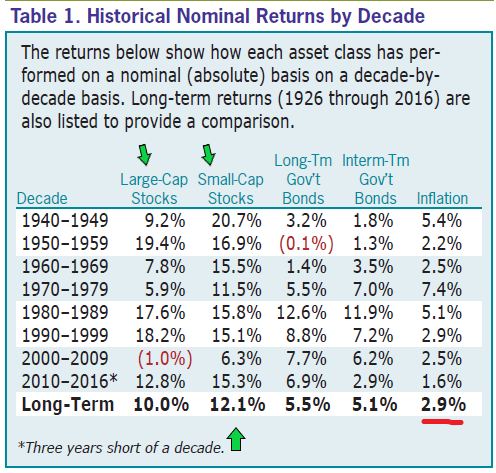

The image from the May 2018 AAII Journal (page 19) tells the story. These are returns BEFORE INFLATION. That means the bond return is far less than 5.5% and does not include bond fund expenses.

Recommendation: If you anticipate you have at least ten years more to live, you may want to minimize your bond investments. I would say no more than 10%. Furthermore, avoid “Target Date Funds” as they are steering you into more-and-more bonds over time.