How Long Will You Last?

The only real answer to this question is “I have no idea.” Frankly, I’m amazed that I am 75 years old. Given my propensity to like donuts, cookies, high-fat foods, and fried chicken, my body seems to continue to function reasonably well.

There are good reasons to think about how long you might live. One of the reasons has to do with income taxes. I just finished e-Filing our federal and Wisconsin income taxes using TurboTax Premier. Our Federal tax bill for 2025 was $30,924 and our Wisconsin income tax bill was $5,485. It would have been far worse if I failed to perform certain tasks every year. While $36,409 was the total amount due, it could easily have been over $50,000.

What Made the Difference?

Three important factors played into keeping our taxes within the realm of reasonable. The first is that we both have ROTH IRA accounts, so there are no income taxes on withdrawals from those accounts. Those investments earn tax-free dividends, tax-free capital gains, and tax-free options trading income.

The second is that I have been diligent in moving assets from my very large traditional IRA account to the ROTH account. While I do pay taxes on those transfers of stocks, including income taxes in 2025, the long-term benefit is reducing my RMD in future years and increasing our tax-free income for the balance of our lives. This income is both dividends and options income.

The third pertains to charitable giving. Cindie and I have long been convinced that God is right. He owns everything and he has put some wealth in our hands to be used for his purposes. God has a treasury that doesn’t go into default and that pays eternal dividends. Before I reached age 71 this giving resulted in lower income taxes by itemizing our deductions. It is now possible to greatly reduce our “income” by giving via Qualified Charitable Distributions (QCD).

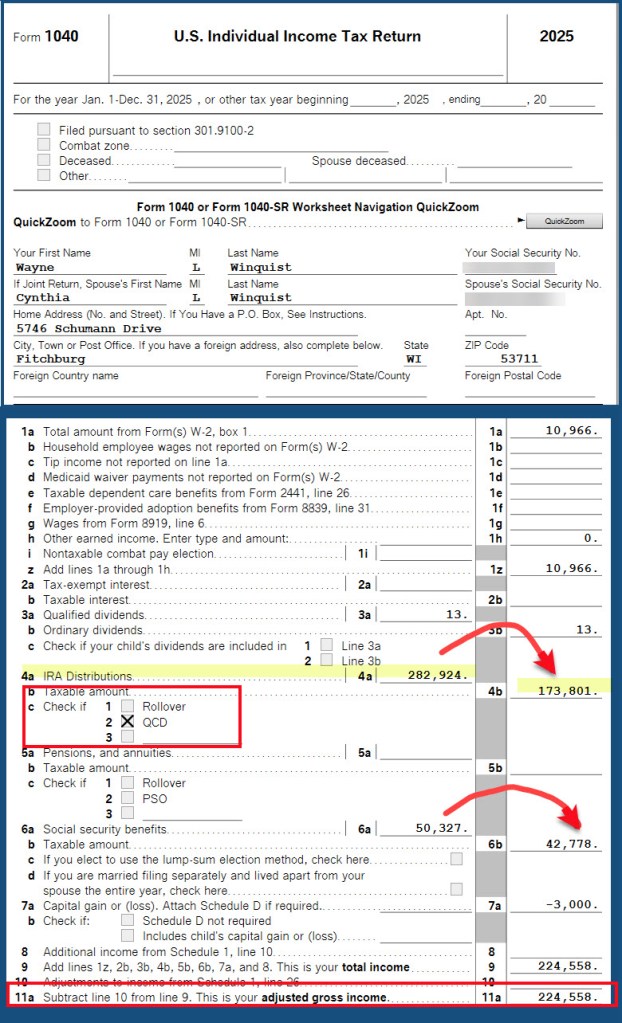

Notice a couple of things in our income tax return. 1) The taxable amount of our traditional IRA withdrawals was considerably less than our IRA withdrawals. This was possible because we gave the maximum QCD gift allowed for 2025 of $108,000. 2) We have to pay income taxes on a large portion of our Social Security. The government gives, but the government takes away. 3) Our AGI (Adjusted Gross Income) was just over $224K. It is important to know that this number can cause your Medicare part B premium to increase, further reducing your Social Security income. This extra tax is called IRMAA. Watch out for her, because she can be very expensive!

What Social Security Thinks About Life Expectancy

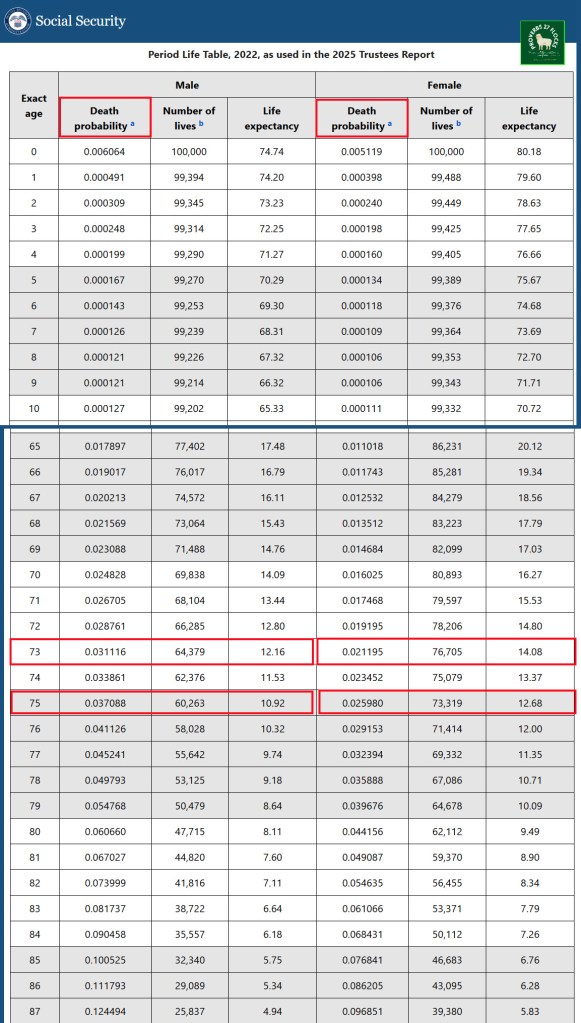

You are going to die. While you don’t know how long you might live, it is reasonably certain that 64,379 men (out of 100,000) will live to age 73. For women it is 76,705. Ladies, are you prepared to live longer? Do your investment decisions mirror that reality? Now that I am 75 I am part of the 60,263 group that made it this far. Of course, these numbers are not hard-and-fast, but they help us understand the probability of living to a certain age based on historical trends.

Because of these realities, what you do with your traditional and ROTH retirement accounts matters greatly when it comes to income taxes in the last decade of your life. This also has a very significant impact on your spouse, should you predecease her. Income taxes become ridiculous for single people (widows and widowers included.)

The RMD Factor

Part of my plan is to keep my traditional IRA RMD below the amount the IRS permits to be given using QCD gifts. For 2026 the QCD limit is $111,000. As my account currently stands based on the current balance, my 2027 RMD will be $67,343.21. This means I will pay $0 in income taxes on my RMD and we will continue to support our local church and other charities. This is far better than itemizing deductions for several reasons.

This also means that I can continue to transfer assets from the traditional IRA to the ROTH during 2026. However, that process has to wait until after I satisfy the RMD with the QCD gifts.

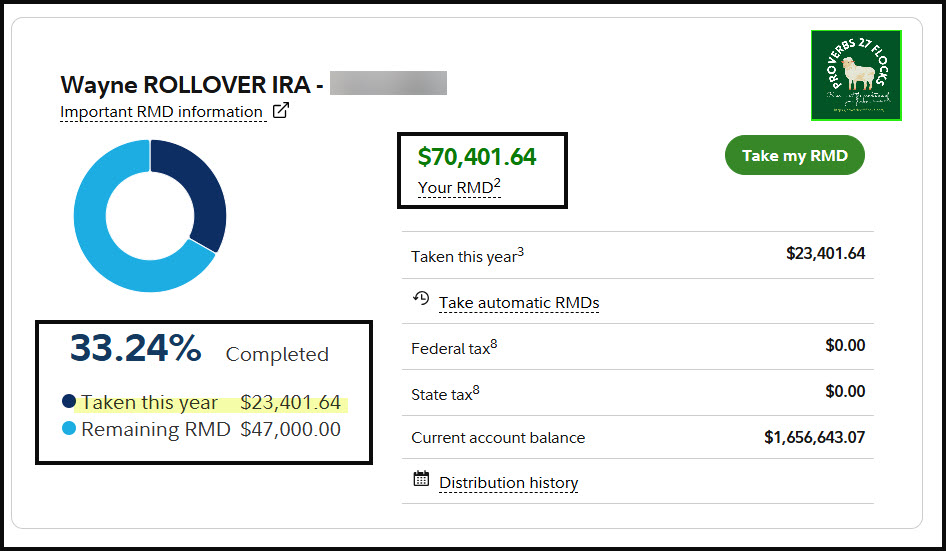

2026 RMD Progress

The following image, from our Fidelity Investments account, shows the RMD for my traditional IRA. Cindie’s RMD is separate and must also be taken during 2026. The amount taken this year, year-to-date is entirely income tax free. The reason is that the entire amount was given using the QCD option.

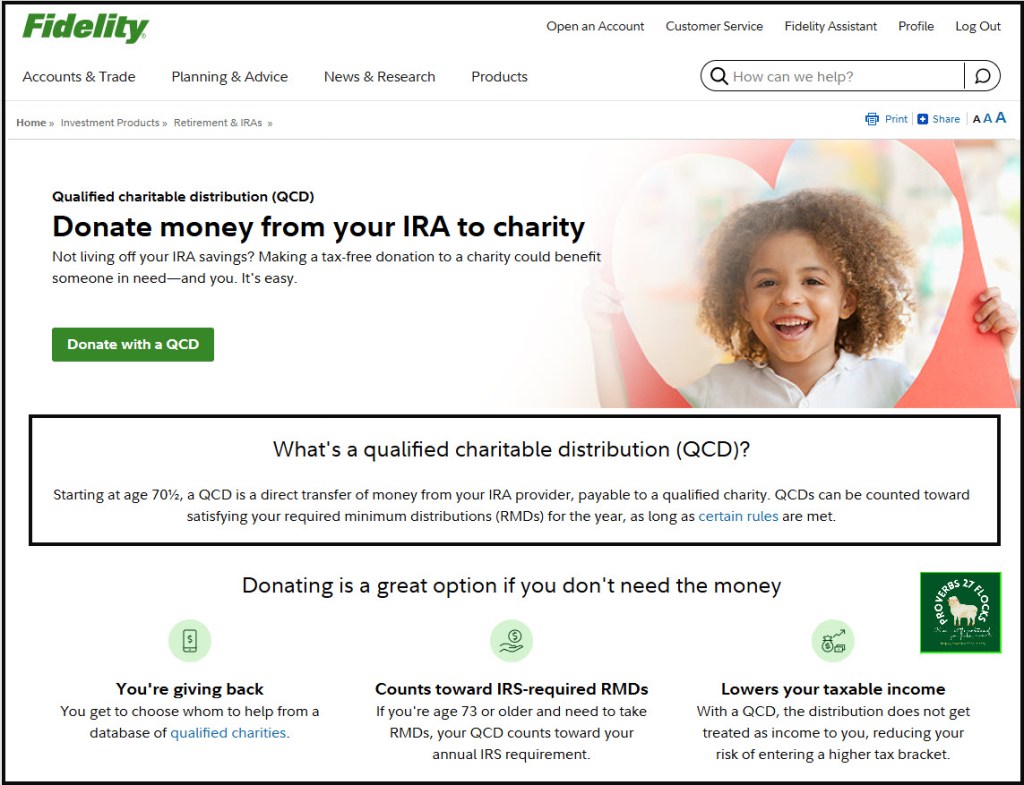

Fidelity Investments Help and IRS excise tax

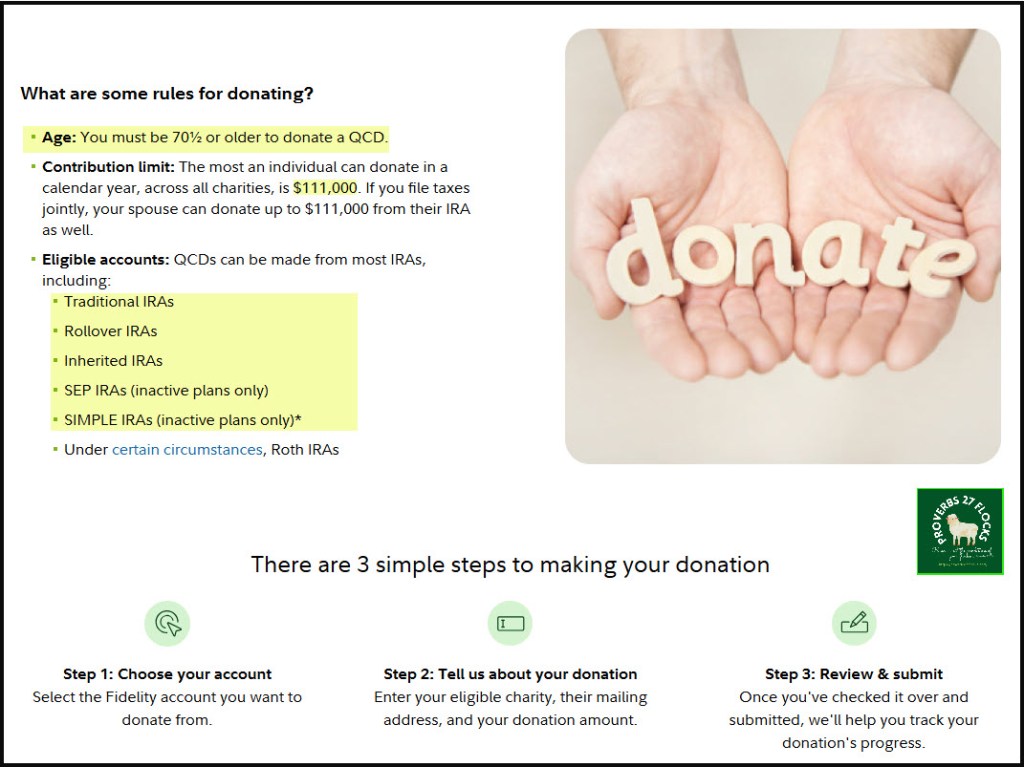

You can find more information about QCD giving on the Fidelity Investment’s website. The following was extracted from Fidelity’s website. Pay special attention to the IRS excise tax!

The IRS taxes RMDs as ordinary income. This means that withdrawals will count towards your total taxable income for the year. Keep in mind that this income increase may push you into a higher tax bracket and may impact the taxes you pay for your Social Security or Medicare.

If you’d like to reduce the effect of RMDs on your taxes, consider making a qualified charitable distribution (QCD). A QCD excludes the amount you donate from taxable income and can be counted toward satisfying your RMD for the year, as long as certain rules are met. A tax advisor can help you determine when to take RMDs and if a QCD is appropriate for your situation.

1.The deadline to complete your RMD is December 31st. In the year you reach age 73 you may elect to delay taking your first RMD until April 1st of the year you reach age 74. If you elect to delay your first RMD until the following year, you will have to take two RMDs in the year you reach age 74. You should consider the tax consequences of taking two RMDs in the same year before electing to delay your first RMD. Beneficiaries eligible to take RMDs from their inherited IRA must begin taking RMD by December 31 of the year following the original owner’s death. If the December 31st or April 1st deadline falls on a weekend or holiday, the deadline to complete your RMD is the business day before.

2. Beginning in 2023 the IRS excise tax on missed RMD amounts is 25%. You may be eligible to reduce the 25% penalty to 10% if the missed amount is removed by the appropriate deadline. Missed RMD amounts for years prior to 2023 are subject to are subject to a 50% excise tax. If you have an annuity, RMD information is provided by your annuity carrier.

3. Distributions from your non-Roth IRAs are subject to federal and, where applicable, state income tax withholding unless you elect not to have withholding apply. Distributions taken before age 59.5 may be subject to a 10% penalty. You can find additional information on withholding and marginal rate tables in IRS Form W-4R.

4. The RMD estimate for inherited IRA and Inherited Roth IRA accounts assumes your were a named beneficiary of the original depositor and the account was funded before December 31st of the year after the original owner’s death (IRS single life expectancy table PDF, (Opens in a new tab)). If these assumptions don’t apply, see which IRS factors apply to you., (Opens in a new tab)

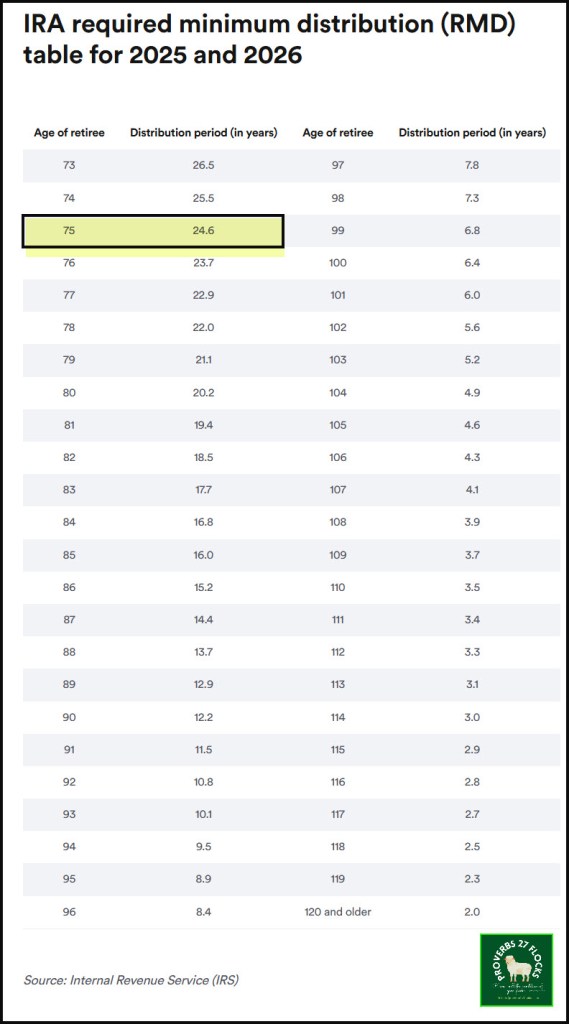

How to calculate your RMD

To calculate your required minimum distribution, simply divide the value of your IRA, 401(k) or other retirement account at the end of last year by the distribution period value that matches your age on Dec. 31 this year. Every age beginning at 73 has a corresponding distribution period, so you must calculate your RMD every year.

Penalty for missing the RMD deadline

It’s your responsibility to ensure you take the full RMD amount by the deadline: The first time you take an RMD, you have until April 1 of the year following the year you turn 73 to do so.

After that, you generally have until Dec. 31 of the current year to take that year’s RMD.

If you haven’t withdrawn the full RMD amount by the deadline, any money not withdrawn faces a 25% penalty. That drops to 10% if the RMD is corrected within two years. In such cases, the IRA owner must fill out IRS Form 5329. See Part IX of this form for the section regarding the additional tax on excess contributions.

Note that if you feel you’ve missed the deadline for a legitimate reason, you can request a waiver from the IRS. For more information, see the waiver of tax for reasonable cause section of the Form 5329 instructions.

Closing Thoughts

Taxes are inevitable. Perhaps not as inevitable as death, but then nothing as inevitable as death. You have a 100% guarantee that you will die. But death is NOT the end. Notice that the IRS table assumes you will die but it doesn’t mention what comes next.

The Bible teaches that death is a transition rather than an end, often described as a sleep or unending torment in hell. It emphasizes that through faith in Jesus, believers can have eternal life and will ultimately be free from death and suffering (John 11:25-26, Revelation 21:4). It is only by God’s grace through faith in the finished work of Jesus that the wrath of God can be satisfied. Good works don’t mean anything before faith.

“For the unsaved, death ends the chance to accept God’s gracious offer of salvation: “People are destined to die once, and after that to face judgment” (Hebrews 9:27).” Got Questions

Seeking Alpha Subscription Information

Of all of the resources I use, the most helpful is Seeking Alpha. If you decide to explore a Seeking Alpha subscription, please use the following link. Seeking Alpha

SEEKING ALPHA INFORMATION AND SUBSCRIPTION

You can also scan this QR Code to get the same information.

Past performance does not guarantee future results, Seeking Alpha does not provide personalized advice, and it is not a registered investment adviser.

We accept advertising compensation from companies that appear on our site. This website represents my opinions, which may not reflect those of Seeking Alpha, and does not constitute an investment recommendation or advice.