Can Your Investments Buy Your Groceries?

In January Cindie and I spent about $600 on groceries. That was more than our December spend of $440. If I had to guess, I think it is normal for us to spend about $500 per month on groceries. Bear in mind that we host a small group from our church, so some of the food is for our guests. This food budget will be important for what I will say later in this post.

Yesterday I had a phone conversation with a friend who is a helpful, quality-focused, remodeling and building contractor. Over the years he has done some remodeling projects on our home. I appreciate the quality of his workmanship. In 2018 he and his wife requested my help to work on their investments. During the last eight years he has asked a lot of good questions, and he has followed my advice.

Yesterday he started to be more proactive in understanding the results he was seeing for some of his positions. These are stocks and ETFs that I purchased for him. He has granted me trading authority on his accounts.

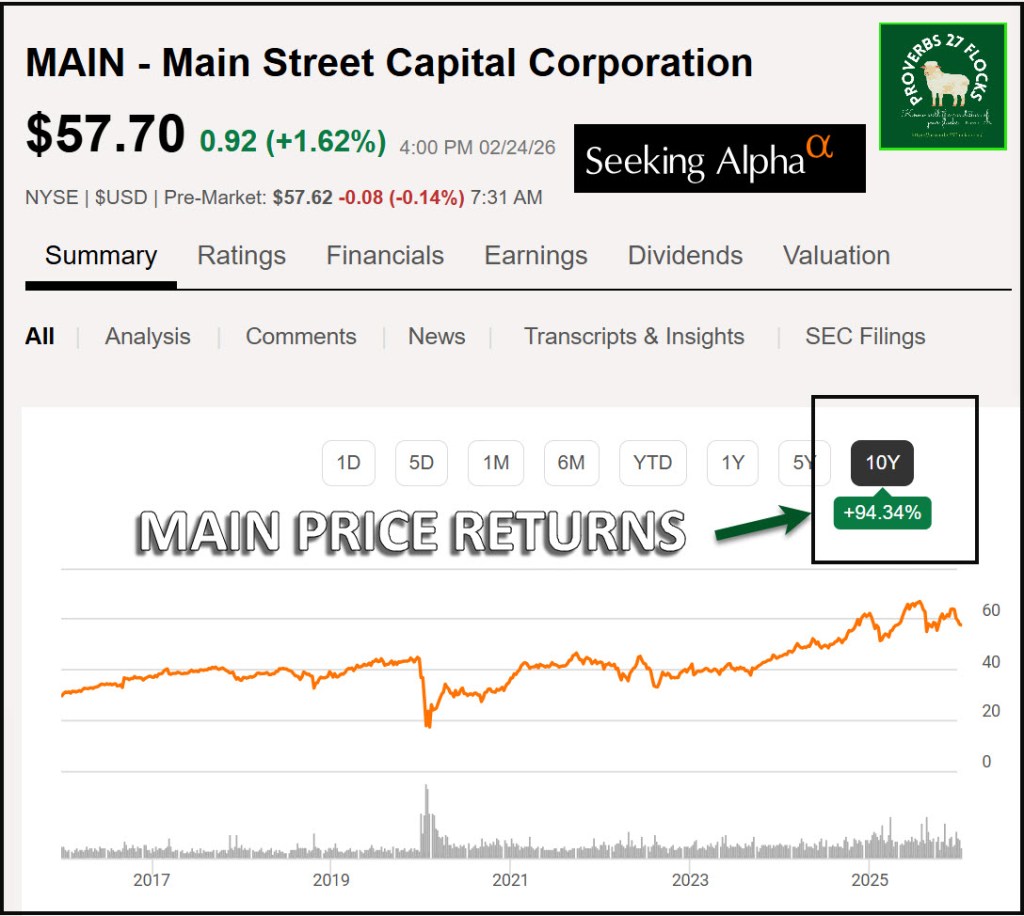

He knew that ten-year returns are one marker of the success of an investment, but he misunderstood the big picture regarding the investment’s ten-year returns. I’m convinced that more than 95% of investors don’t understand the numbers they see when they log in to Fidelity’s website and review their positions. He concluded that the 10-year returns on the investments in his ROTH IRA were not worthy of his investment dollars.

This is a very common misconception. Most displays show price returns, even on your statements. However, if you are not automatically reinvesting dividends your web view or your statement will not reflect total returns.

What Is Missing?

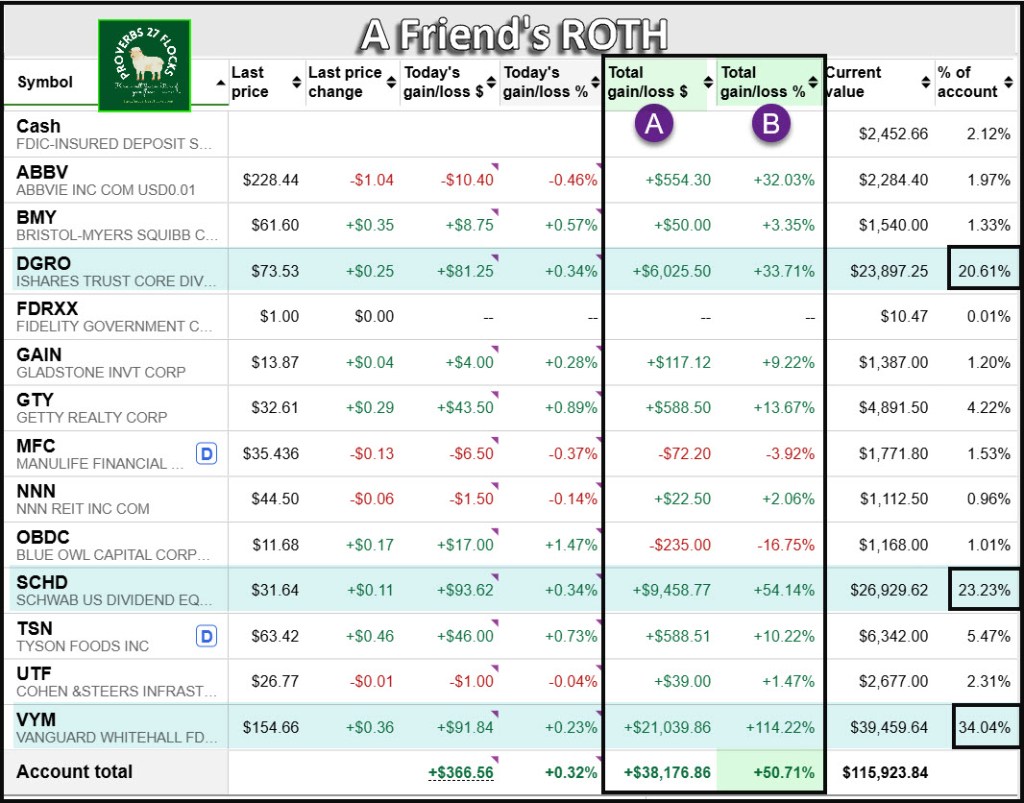

When you look at this image, especially the columns that say, “Total gain/loss $” and “Total gain/loss %” you cannot believe what it tells you. Your statement is true and accurate but only if you understand it is focused on price returns. It is lacking one key element for positions where the dividend is not automatically reinvested. It lacks the dividend income received during the life of the investment.

For example, the total gain for GTY is more than 13.67% for this particular holding. This number does not include the quarterly dividends being paid. It also would not include any options income.

A surprising number of investors don’t understand the power of dividends in a portfolio of investments. They think dividend investments cannot and will not outperform the overall market. That is true for some dividend-focused investments, but it certainly is not true for many good investments. MAIN is one such investment. It has outperformed the S&P 500 over the last ten years.

Ask: What are your True Returns?

There are two pieces for most investors and three pieces for investors who trade options contracts. If you are in the “most investors” category, then you returns are the profit or loss from the sale of an investment (capital gain or loss) plus any dividends you received during the time you owned the investment. The first part is a price return on your investment. If you paid $10/share and received $20/share when you sold, you made a profit of $10 per share. That is a capital gain.

However, if the investment also pays a dividend, then the dividend is part of your return. Let’s assume the annualized dividend is $0.25 per share. If you held the investment for four years you also received an additional $1.00 per share of income. That should be added to your total gain. That is your total return. That is not shown in the Fidelity view that says “Total gain/loss $.”

Furthermore, if you add income from options trades into the mix, your profit can increase substantially. In fact, it is possible to earn income on non-dividend paying stocks. Those options profits are not shown either.

Main Street Capital Corporation Returns

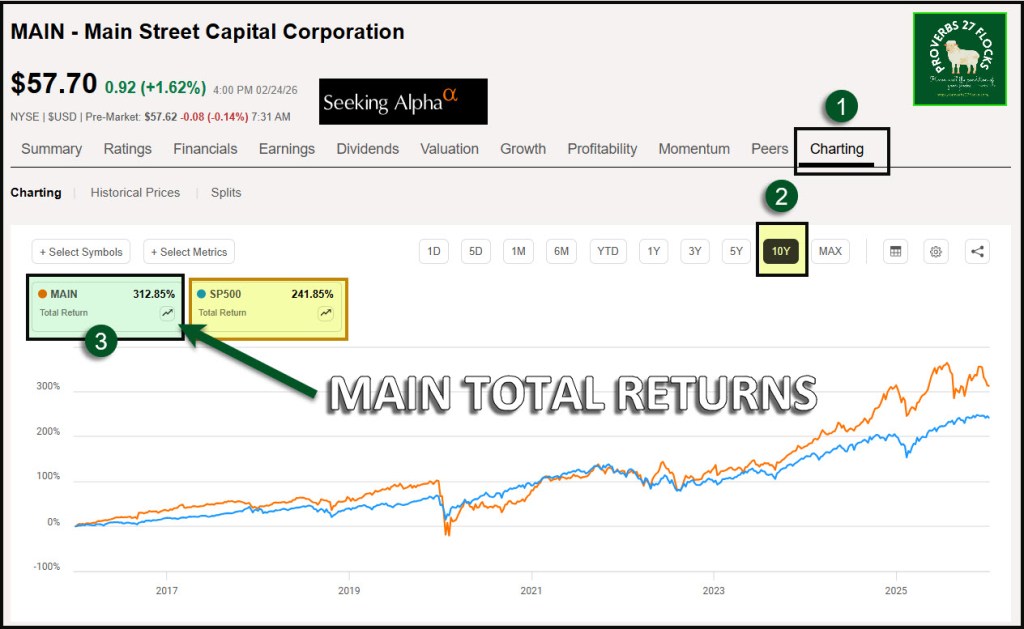

If, for example, you look at the ten-year returns for business development company MAIN (Main Street Capital Corporation), you could conclude that the 10-year returns are 94.34%. This is an erroneous conclusion because it misses a huge part of why MAIN can be a huge benefit in a retirement portfolio. The ten-year total returns for MAIN are almost 313% compared to the 242% total returns for the S&P 500. In other words, even though the untrained eye thinks MAIN is a losing battle, that untrained eye is blinded to the things MAIN provides investors: immediate cash plus outstanding returns.

Main Street Capital Corporation Dividend

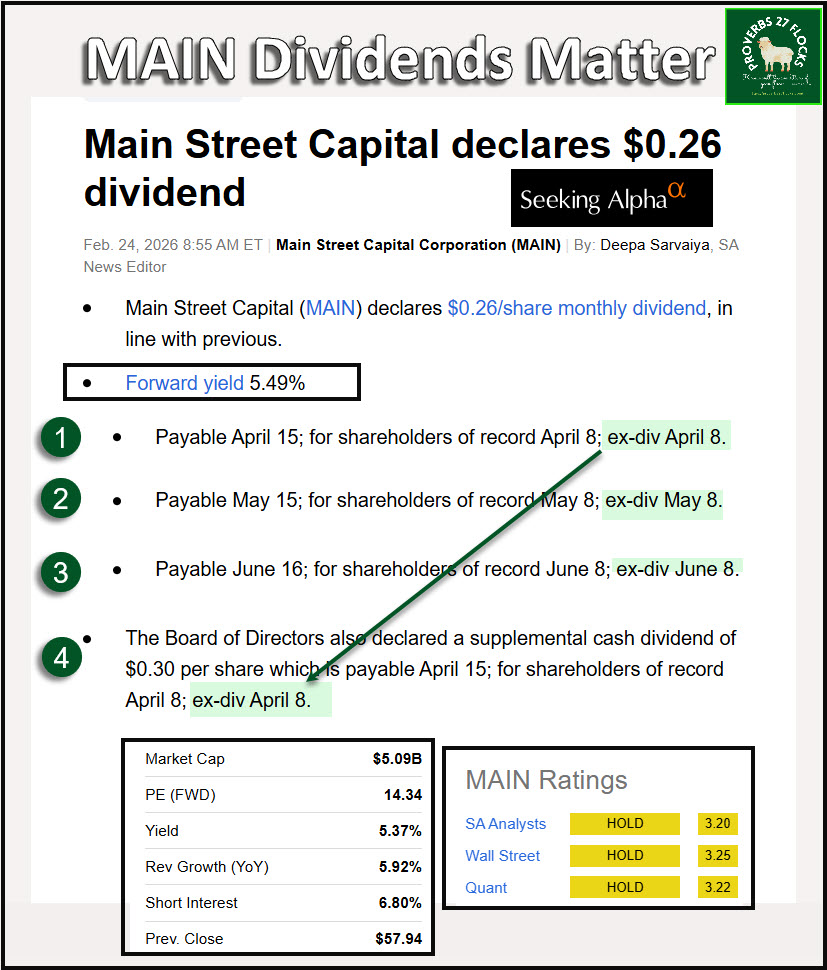

The most recent dividend announcement included the following four dividends. Three of them are monthly and are $0.26 per share. The last one is “supplemental” and it is $0.30 per share. Supplemental dividends are unique and should not be considered repeatable. However, they are a nice present when they are paid. Here are the four announcements:

- Payable April 15 for shareholders of record April 8; ex-div April 8.

- Payable May 15 for shareholders of record May 8; ex-div May 8.

- Payable June 15 for shareholders of record June 8; ex-div June 8.

- The Board of Directors also declared a supplemental cash dividend of $0.30 per share which is payable March 27 for shareholders of record March 20; ex-div March 20.

Cindie and I own 2,200 shares of MAIN. Therefore, the supplemental dividend we will receive on March 27 will be $660. Then, each month from April through June we will also receive a monthly payment of $572. Remember our January grocery spend? Think about these numbers in your grocery budget each month. How much do you spend on groceries? Will your investments cover the cost of groceries in retirement?

More About MAIN

In February of last year I wrote about MAIN. The title of the post was “Will MAIN’s Dividend Decrease in 2025?” Here is a link if you want to read that one: MAIN DIVIDENDS

In May 2025 I wrote about MAIN again – “Main Street Capital Corporation Dividends (MAIN)” MAIN AGAIN

Caution for the Novice

Not all BDCs are good investments. A Business Development Company (BDC) is not without risk. MAIN is a BDC. A BDC is a type of investment firm that primarily invests in small and mid-sized businesses, providing them with capital and managerial support to help them grow. BDCs are publicly traded and must adhere to specific regulations, including investing at least 70% of their assets in eligible companies.

The BDC Risks

BDCs invest in a range of securities that can be influenced by fluctuations in market conditions, affecting portfolio values and income. They often invest in smaller or distressed companies, which may have a higher chance of defaulting on their debt obligations compared to larger firms. BDCs may hold illiquid investments that can be hard to sell, especially during adverse market conditions, potentially affecting their ability to meet obligations.

Changes in interest rates can affect the cost of borrowing and the yield on investments, impacting profitability and dividend payments. BDCs are subject to various regulations that can change, affecting their operations and compliance costs. Some BDCs may heavily invest in specific industries or sectors, which can lead to increased vulnerability to downturns in those areas. The performance of a BDC can significantly depend on the expertise of its management team. Poor management decisions can negatively impact returns. Finally, since BDCs are required to distribute at least 90% of taxable income as dividends, if profits decline, their ability to maintain dividend payments may be compromised.

Conclusion

If you belong to the camp that believes dividend investors are missing out on the real action, then perhaps you don’t fully understand the power of dividend investing. Of course not all dividend investments are good ones. However, you can say the same things about stocks and ETFs that don’t pay a dividend.

Seeking Alpha Subscription Information

Of all of the resources I use, the most helpful is Seeking Alpha. If you decide to explore a Seeking Alpha subscription, please use the following link. Seeking Alpha

SEEKING ALPHA INFORMATION AND SUBSCRIPTION

You can also scan this QR Code to get the same information.

Past performance does not guarantee future results, Seeking Alpha does not provide personalized advice, and it is not a registered investment adviser.

We accept advertising compensation from companies that appear on our site. This website represents my opinions, which may not reflect those of Seeking Alpha, and does not constitute an investment recommendation or advice.

If you have any questions or problems getting connected to Seeking Alpha, reach out to them with this email address: subscriptions@seekingalpha.com