When Preparing to “Retire” Think Long-Term

A surprising number of Americans live life as if they don’t have to plan ahead. As a result, far to many individuals (really most!) enter retirement with less than $100,000 in retirement savings. There are many costs associated with retirement that are hard to avoid. There are the normal costs of living, which are going up as inflation eats away at the value of our currency. But there are also hidden costs that are often covered or mostly covered as a part of working for a business or for the government.

It is easy to grow accustomed to health care, hospitalization, eye care, dental care, and a host of other benefits during the working years. When you leave the workforce, it will be necessary to decide what you will do and what it will cost to keep from having health care catastrophic events from making life very complicated.

Getting and Listening to Advice

Many ask for advice, and some listen. An even smaller portion of those who listen put a plan in place based on the advice they received. I’ve seen this many times in helping others with spiritual, financial, and relationship issues. The book of Proverbs even offers advice about advice.

“The way of a fool is right in his own eyes, but a wise man listens to advice.” Proverbs 12:15

“By insolence comes nothing but strife, but with those who take advice is wisdom.” Proverbs 13:10

“Listen to advice and accept instruction, that you may gain wisdom in the future.” Proverbs 19:20

Some Free Retirement Advice Regarding Healthcare Insurance

I have been “retired” for over ten years. As I have walked down this path I have had the benefit of looking at many aspects of retirement and have seen some common questions about entering the retirement years. While I don’t know everything about everything related to insurance in retirement, let me offer some advice.

Take Care of Your Health Today

I used to joke that I got an annual physical every five years. That doesn’t work well after you reach your sixties. I also ate too much of the wrong stuff (and sometimes still do) and I was carrying 30 pounds too much on my body in places where extra weight isn’t helpful. It is amazing how many things about my health improved when I started eating more sensibly. Yes, I still indulge in Oreos, pies, and my homemade gluten free dark chocolate banana bread. However, instead of eating a row of Oreos, I will be satisfied with two or three. I also consume more fish, more fresh vegetables, and use care when ordering at a restaurant.

Decide What You Don’t Need

Example #1: Vision Care

Every time I do the math for eye care insurance coverage, I conclude it is a way to make the insurance company win. If you do the math for eye care insurance, you might think twice about paying for it. For example, I looked at Humana’s “Vision Plus” plan that costs $14.49 per month. That is about $174 per year. This plan and others have different copays, deductibles, inclusions, and exclusions. I found some that range from $12.29 per month with various “allowances” through $25.65 per month ($307.80/year).

If you do annual eye exams, you might break even. However, many people don’t have that kind of discipline. The insurance company is not giving you anything for “free.” They do the math. You should too. Therefore, Cindie and I do not carry eye care insurance. When I went to get my eyes checked last year, the cost for the exam, new frames, and the best progressive lens available, I paid $645.50. Medicare refunded $72 of that amount, so my actual cost was $573.50. In 2020 Cindie and I both had eye examinations and got new glasses and prescription lens replacements. Our costs were about $558 each.

If I do the math using eye care every three years, the three-year cost of the 2020 solution was $186 per year for my vision care. If you compare that to insurance that costs $174 per year and add in the copays and deductibles, you should see that being self-insured can make good financial sense.

Example #2: Dental Care

This year I had to have a crown replaced. That was costly to the tune of $1,712. However, our normal annual twice-per-year dental exams, X-rays, and cleaning cost a total of $869. Dental Health Associates in Fitchburg gives us a 10% deduction paying with cash instead of a credit card.

Delta Dental offers “two adults” an “Ultimate Plan” for $184/month, an “Elite Plan” for $154/month, an “Enhanced Plan” for $108/month, a “Clear Plan” for $102/month, and a “Basic Plan” for $62.44 per month. I could pick the one in the middle: the Enhanced plan.

This plan will cost $1,296 per year, which is clearly more than our normal annual dental care costs. But read the fine print. “Enhanced Plan Description; 100% preventive coverage, plus cost-sharing for restorative and major services; Office visit copayment: None; Plan dollar maximum per person per year $1,000 and Deductible per calendar year $50 per person; (Does not apply to Diagnostic & Preventive services, such as cleanings and X-rays). An annual contract is REQUIRED.

Furthermore, the “Enhanced Plan” only covers 50% of the cost of the crown and a “12 month waiting period may apply.” So if I pay for the insurance, I still pay for half of the crown. Ouch! The “Elite Plan” has the same crown coverage, and the “Ultimate Plan” is only slightly better.

The Ultimate plan would cost $2,208 per year, and the Elite plan would set you back $1,848 per year. You might decide this type of insurance is worth covering the surprises like crowns. I think the insurance company wins.

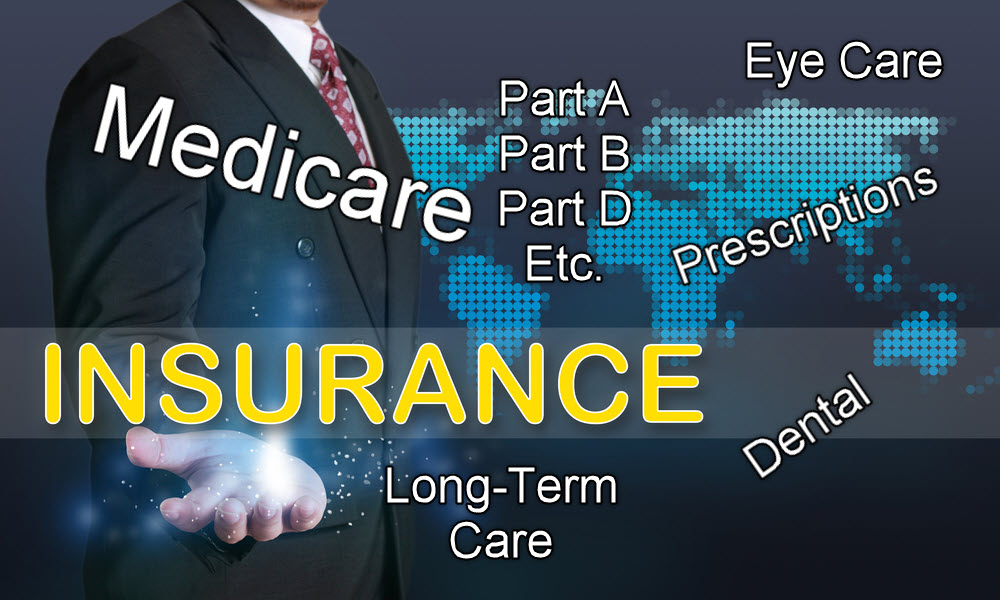

Health Care Coverage In Retirement

This, I believe, is a necessity for most people. When you reach age 65 you must enroll in Medicare, and it is prudent to purchase a Medicare Part B supplement policy. You also need to have a prescription drug “Part D” policy that has a separate premium. In my next post I will discuss what we did and why I think it is not only good coverage, but also cost-effective coverage in retirement. The total of all three (six to include both Cindie and me) policies is just over $8,000 per year. I will break that down in the next blog post.

If you want to earn enough from your retirement assets, assuming a 5% dividend, then your retirement account balance to cover your health care should be $160,000. That balance is ONLY for health care costs. Of course, if you also receive Social Security, that can cover the Medicare Part A premium. In fact, Social Security automatically deducts your Medicare premium from your Social Security each month. Realize that what your Social Security statement tells you is your expected monthly income is BEFORE the Medicare premium deduction. You don’t get to keep the whole wad.

Suggestions for Vision and Dental Care

Pay yourself and then use your own system to pay for the costs of dental and vision care. When it comes to dental and vision care, set aside $200 per month in a savings account that pays you 3-4% in interest. Then pay cash for the care you receive (if a cash discount is offered.) If I had to guess, your savings will grow using this simple discipline. If you pay the insurance company, remember that they are not dummies. They need to make a profit.

All scripture passages are from the English Standard Version except as otherwise noted.