Charitable Giving is a Priority

Back in January I wrote a series of posts about my 2023 goals. The third goal flowed from the first goal. The first goal for 2023 was to focus on the glory and wisdom of God. Every other goal will flow from that perspective. The second goal was a dividend income goal. The goal was 9% growth for 2023. That may or may not be accomplished. I will know on December 31. That goal might seem self-focused as it might look like an effort to build bigger barns to store temporary treasure. The reality is, I hope, to add more fuel to the third goal. That goal is giving.

Recently someone got me curious about another IRS-related acronym: QCD. QCD is something that becomes a useful tool in retirement for those with traditional IRA accounts. QCD is the abbreviation for “Qualified Charitable Giving.”

Today I spent a portion of my day getting ready to use a legal way to reduce our income taxes and increase our giving.

What I Discovered About QCDs and RMDs

It is good news. Rather than withdrawing cash from my traditional IRA, paying the income tax, and then giving the remainder to our church or to any other legitimate charity, I can have Fidelity send a check to the church or charity without withholding taxes. In other words, if I were to give around $55,000 next year to the organizations we support, I would save at least $10,000 in income taxes. In other words, I can increase our giving from $45,000 to $55,000 just by changing the way we give. Here is what the IRS says regarding this opportunity:

Qualified charitable distributions allow eligible IRA owners up to $100,000 in tax-free gifts to charity. (IRS)

“IR-2023-215, Nov. 16, 2023 – WASHINGTON —The Internal Revenue Service today reminded individual retirement arrangement (IRA) owners age 70½ or over that they can transfer up to $100,000 to charity tax-free each year. These transfers, known as qualified charitable distributions or QCDs, offer eligible older Americans a great way to easily give to charity before the end of the year. And, for those who are at least 73 years old, QCDs count toward the IRA owner’s required minimum distribution (RMD) for the year.” LINK

An Added Bonus

Because of my age, I have to start taking RMDs next year. It is likely that my RMD will be close to $70,000. If I use the QCD approach, I fulfill at least $55K of my RMD requirement. That would mean that I only have to take $15,000 in taxable income.

This creates an amazing opportunity for about $100,000 in ROTH conversions from my traditional IRA, which works in our favor to reduce the 2024 RMD. This also makes it possible to reduce our exposure to the Medicare IRMAA premium costs.

But the best part of this whole idea is that we can give more, by simply avoiding income taxes using wise application of income tax law. We want to be good stewards of the wealth God has given us, and the QCD-RMD approach helps us do just that.

Fools Try to Rob God

In the Old Testament, one of the last words from God was to his people. They were far from perfect, and they revealed their sinfulness in many different ways. One way was to neglect things that God said were the priority. Someone who claims to be a Christian should be like the Savior. This includes great generosity at personal cost. Here is what God said through Malachi:

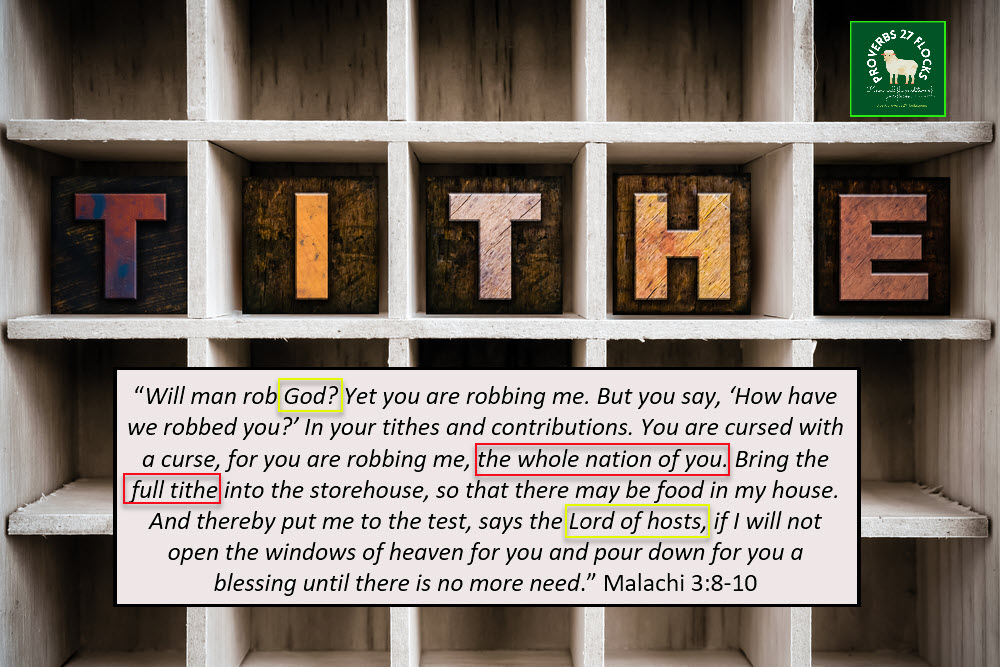

“Will man rob God? Yet you are robbing me. But you say, ‘How have we robbed you?’ In your tithes and contributions. You are cursed with a curse, for you are robbing me, the whole nation of you. Bring the full tithe into the storehouse, so that there may be food in my house. And thereby put me to the test, says the Lord of hosts, if I will not open the windows of heaven for you and pour down for you a blessing until there is no more need.” Malachi 3:8-10

Lest you think giving is just an “Old Testament Idea”, it is worth the time to read what the Apostle Paul said to the Corinthian church in 2 Corinthians 9:6-15.

Conclusion and Suggestion

If you believe in giving, and if you are at least 70.5 years old (or if some day you are going to be that age) you may want to think about adding QCD to your alphabet soup of helpful abbreviations.

It doesn’t hurt to talk to your broker about this. Fidelity has some great options for QCDs, and I already used their online functionality to send my first gift, saving $1,000 in income tax, thus giving the charity an additional $1,000 over what I would have been able to do without this approach.

I also requested checks from Fidelity for my traditional IRA. I can then write checks to any charity that is willing to provide me with a letter acknowledging the gift. Bear in mind, however, that the gifts given this way are NOT allowed as an additional SCHEDULE A deduction. That would be double-dipping. Therefore, a charity or church needs to separate regular giving from QCD giving on any statements they provide.

As with previous posts in this series, as I continue my tax reduction journey, I hope to be able to explain what I did and why I did it. I also plan to share some links for various resources applicable for those who are interested in their own tax situation.